How to Lower Car Insurance: 10 Proven Money-Saving Tips

Most Americans overpay for auto insurance simply because they don’t know which levers to pull. Insurance companies offer dozens of discounts they rarely advertise, from bundling policies to completing defensive driving courses to installing anti-theft devices.

Beyond discounts, strategic decisions about deductibles, usage-based programs, and dropping unnecessary coverages can slash your premiums by hundreds or even thousands annually. These tactics work regardless of your age, driving record, or location, and complement the broader understanding of how insurance costs and coverage options work together to protect your financial interests.

1. Shop around like your wallet depends on it

The single most effective way to lower your car insurance costs is comparing quotes from multiple companies. Rates for identical coverage can vary by $500 to $1,500 annually between insurers and I’m not exaggerating even slightly.

Insurance companies use different formulas to calculate risk. One company might weight your age heavily while another focuses more on your vehicle type or credit score. What makes you expensive to insure at Company A might be less important to Company B.

Get quotes from at least five different insurers. Include national brands like GEICO, Progressive, State Farm, and Allstate. Also check regional companies that operate in your state because regional insurers sometimes offer better rates since they understand local conditions better than national chains.

Price variation comparison for identical coverage:

Same driver, same car, same coverage limits – but drastically different prices across five major insurers:

| Insurance Company | Annual Premium | Difference from Lowest |

|---|---|---|

| GEICO | $1,350 | Lowest price |

| Progressive | $1,480 | +$130 |

| State Farm | $1,650 | +$300 |

| Allstate | $1,850 | +$500 |

| Farmers | $2,400 | +$1,050 |

Based on quotes for 35-year-old driver, Honda Accord, 100/300/100 coverage, $1,000 deductible

That’s a difference of $1,050 between the highest and lowest quote for exactly the same protection. This is why shopping around isn’t optional if you want to save money.

The comparison process that actually works:

Request identical coverage from each company and this part is crucial. Specify the exact liability limits, deductibles, and coverage types. Otherwise you’re comparing apples to oranges and won’t identify the true cheapest option.

I learned this the hard way years ago. Got three quotes that looked wildly different but then realized one had $500 deductibles while another had $1,000 deductibles. Once I standardized everything the cheapest option changed completely.

Set a calendar reminder to reshop every six months. Insurance companies constantly adjust their pricing algorithms and risk models. The cheapest company this year might be expensive next year and loyalty doesn’t pay in the insurance business.

Online comparison tools help but don’t rely on them exclusively. Some insurers don’t participate in comparison sites. Calling companies directly or working with an independent agent often reveals options the online tools miss.

Real savings example:

I was paying $1,900 annually with my insurer of eight years. Got quotes from five companies. Same exact coverage ranged from $1,350 to $2,400. Switched to the $1,350 option and saved $550 annually. Took maybe three hours total including the phone calls.

2. Bundle policies for automatic savings

Combining your auto and homeowners or renters insurance with one company typically saves 15% to 25% on your auto premium. The discount varies by company but it’s almost always worth doing.

I bundle my car and homeowners insurance and save about $400 annually. Even if you’re renting, adding a $15 monthly renters policy can trigger enough of an auto discount to make the renters policy essentially free while protecting your belongings.

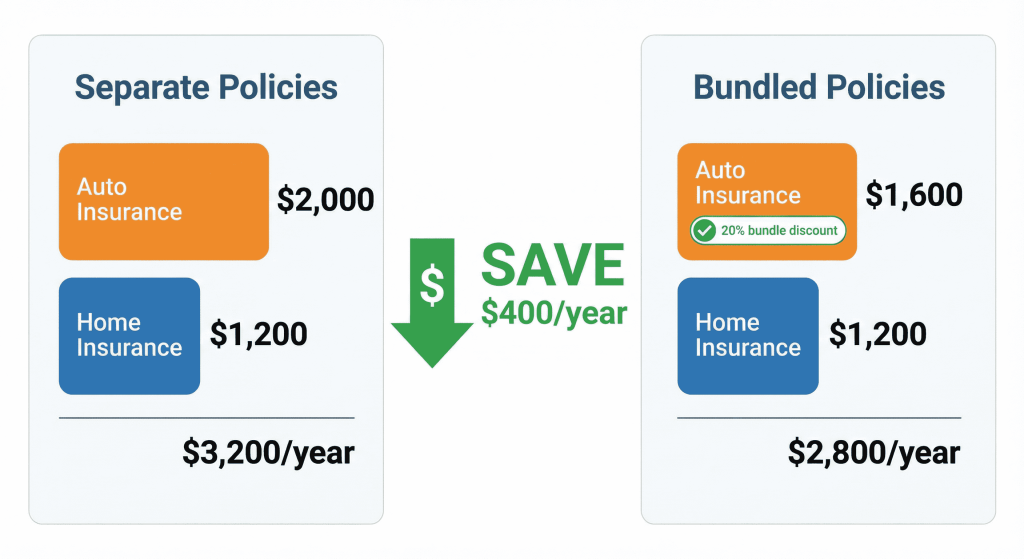

How bundling affects your total insurance costs:

Looking at a typical scenario with $2,000 auto insurance and $1,200 home insurance purchased separately, you’d pay $3,200 total annually. Bundle them together and the auto portion drops to $1,600 with a 20% discount while home insurance stays at $1,200. Your new total is $2,800, saving you $400 per year.

Some insurers also offer bundling discounts for combining auto with life insurance, umbrella policies, or motorcycle coverage. Ask about every possible bundle because agents don’t always volunteer this information.

The math occasionally doesn’t work though. Sometimes the bundled price exceeds buying separate policies from different companies. Run the numbers both ways but bundling wins most of the time.

My sister learned this when she bought her house. Her auto insurer quoted $2,800 for bundled auto and home. Separate companies quoted $1,400 for auto and $900 for home insurance. She saved $500 by not bundling. Always verify the math.

3. Raise your deductibles strategically

Your deductible is what you pay out of pocket before insurance kicks in. Raising your deductible from $500 to $1,000 can cut your collision and comprehensive premiums by 30% or more.

The key word is strategically though. Only raise deductibles to amounts you can actually afford if something happens. Saving $20 monthly doesn’t help if you can’t come up with $1,000 after an accident.

The deductible impact on annual premiums:

| Deductible | Annual Premium | Monthly | Savings vs $250 |

|---|---|---|---|

| $250 | $2,150 | $179 | — |

| $500 | $1,850 | $154 | $300/year |

| $1,000 | $1,500 | $125 | $650/year |

| $2,000 | $1,350 | $113 | $800/year* |

*Requires having $2,000 cash available if something happens

I keep a separate savings account with enough to cover my deductibles. It gives me peace of mind and lets me carry higher deductibles for lower premiums. The money I save on premiums goes straight into that deductible fund.

Consider different deductibles for collision versus comprehensive. You might carry a $1,000 collision deductible but a $500 comprehensive deductible if you live in an area with high theft or hail risk.

Going above $1,000 deductibles delivers diminishing returns. The premium savings between $1,000 and $2,000 deductibles is usually modest compared to the extra risk you’re assuming. I tried a $2,000 deductible once and only saved an extra $150 annually. Not worth it for my situation.

4. Squeeze every possible discount from your insurer

Insurance companies offer dozens of discounts but they won’t always advertise them all. You need to ask specifically about each one and I mean really push on this.

Stacking discounts for maximum savings:

The power of combining multiple discounts is where real money gets saved:

Safe driver discounts reward clean records. No accidents or violations for three to five years typically earns 10% to 20% off, which is $215 to $430 annually for the average driver. This one rewards good behavior you should practice anyway.

Good student discounts help young drivers and every bit counts when you’re paying $4,000+ annually for a teenager. Students under 25 who maintain a B average or better often qualify for 8% to 15% discounts, saving $320 to $600 yearly. Provide report cards or transcripts as proof.

Low mileage discounts apply if you drive under 7,500 to 10,000 miles annually, saving 5% to 15% or $100 to $300 per year. Working from home or having a short commute makes you eligible.

My defensive driving course experience:

I took an online defensive driving course that took about six hours total spread over two evenings. Cost me $35. My insurance dropped by $110 annually for the next three years. That’s $330 in savings for $35 and six hours of my time.

Multi-vehicle discounts save 10% to 20% when you insure two or more cars on the same policy. That’s $200 to $400 annually and it’s one of the easiest discounts to claim if you have multiple vehicles in your household.

Safety feature discounts reward automatic emergency braking, anti-lock brakes, airbags, and electronic stability control. Newer vehicles often qualify for multiple equipment discounts automatically, saving 5% to 15% or $100 to $300 yearly.

Professional affiliation discounts exist for many occupations, industries, alumni groups, and professional associations. Engineers, teachers, military members, and countless other groups qualify for discounts at various insurers. Always ask because this one surprises people. These can save 5% to 15% or $100 to $300 annually depending on the group.

5. Try usage-based insurance programs

These programs monitor your driving through a smartphone app or plug-in device. Safe drivers can save up to 30% to 40% on their premiums which is substantial.

The device or app tracks factors like hard braking, rapid acceleration, speed, and time of day you drive. Night driving and excessive speeding hurt your score. Smooth driving during daytime hours helps your score.

How usage-based insurance scores your driving:

Your driving score gets calculated from multiple factors with different weights. Smooth braking events earn you 30 points toward your total score representing the biggest factor. Maintaining steady speeds without rapid acceleration adds 25 points. Driving during daytime hours between 6am and 10pm contributes 20 points. Staying within speed limits gives you 15 points. Minimal harsh cornering adds 10 points. Combined, a perfect score of 100 points earns you the maximum 40% discount.

I was skeptical at first but after trying Progressive’s Snapshot program I saved $280 annually. If you’re confident in your driving habits it’s worth considering.

The privacy trade-off bothers some people which is completely valid. The apps and devices collect detailed information about where you drive, when you drive, and how you drive. Read the terms carefully to understand what data gets collected and how it’s used.

What the monitoring revealed about my driving:

When I tried the program, I learned I brake harder than I thought. The app dinged me for hard braking events I didn’t even notice. Made me more aware of my driving habits and I consciously started braking earlier and more gradually. My score improved and my driving probably got safer too.

6. Improve your credit score for insurance savings

In most states your credit score significantly impacts your insurance premium. Improving your credit from fair to good can reduce your insurance costs by hundreds of dollars annually.

Insurance companies use credit-based insurance scores which differ slightly from regular credit scores but correlate closely. People with better credit scores file fewer claims according to insurance industry data.

Credit score impact on insurance premiums:

| Credit Score | Annual Premium | Impact |

|---|---|---|

| Exceptional (800+) | $2,150 | Baseline rate |

| Very Good (740-799) | $2,408 | +12% |

| Good (670-739) | $2,688 | +25% |

| Fair (580-669) | $3,225 | +50% |

| Poor (below 580) | $4,300 | +100% (2x cost) |

Pay all bills on time. Payment history represents the biggest factor in your credit score. Set up automatic payments to avoid missing due dates.

Reduce credit card balances. High utilization rates hurt your score. Aim to keep balances below 30% of your credit limits. Paying down debt improves your score relatively quickly.

Check your credit report for errors. Mistakes happen and incorrect negative items drag down your score. You can dispute errors with credit bureaus and get them removed.

My personal credit improvement story:

I improved my credit score from 680 to 760 over two years and my insurance premium dropped by about $350 annually. That’s $350 every year going forward just for managing my credit better. The same credit improvement also helped me get better rates on my mortgage refinance, so the benefits extended beyond just insurance.

7. Drop coverage you genuinely don’t need

This requires careful analysis but some coverage might be redundant or unnecessary for your situation.

If you own an older car outright, collision and comprehensive might cost more than they’re worth. Run the math carefully. If your car is worth $3,000 and collision plus comprehensive costs $600 annually with a $1,000 deductible, you’re paying 20% of the vehicle’s value annually to potentially receive a maximum $2,000 benefit after the deductible.

When to drop collision and comprehensive coverage:

My rule of thumb is if your car is worth less than 10 times your annual collision and comprehensive premium, consider dropping those coverages. Self-insure by putting the premium savings into a car replacement fund.

If you have excellent health insurance, you might not need high medical payments or PIP limits. Check whether your health insurance covers auto accidents before reducing these coverages but many people carry duplicate protection without realizing it.

I discovered I had $10,000 in medical payments coverage on my auto policy but my health insurance already covers auto accidents with a lower deductible. I dropped the medical payments coverage and saved $85 annually. That’s $85 I was wasting on duplicate protection.

Rental reimbursement coverage is convenient but often expensive relative to the benefit. If you have access to alternative transportation or can rent a car at market rates if needed, this add-on might not make sense. I dropped rental reimbursement and save $35 annually. When I needed a rental after an accident I paid $200 out of pocket but I’d already saved $140 over four years of not having the coverage.

8. Take advantage of low mileage programs

If you work from home or simply don’t drive much, tell your insurance company. Many offer significant discounts for drivers putting fewer than 7,500 or 10,000 miles annually on their vehicles.

Annual mileage and your premium:

| Driver Type | Annual Miles | Premium |

|---|---|---|

| Heavy commuter | 20,000+ | $2,400 |

| Average driver | 12,000-15,000 | $2,150 |

| Low mileage | Under 10,000 | $1,850 |

| Very low mileage | Under 5,000 | $1,400 |

The difference between heavy and very low mileage is $1,000 annually in savings.

Some companies now offer pay-per-mile insurance where you pay a low base rate plus a per-mile charge. If you’re only driving 5,000 miles yearly this can save hundreds compared to traditional pricing.

Metromile pioneered this model but other companies now offer similar programs. You install a device that tracks mileage and pay accordingly. If you drive more than expected in a given month your rate increases but if you drive less you pay less.

A friend’s pay-per-mile success:

A friend switched to Metromile when she started working from home during the pandemic. Her traditional insurance cost $1,400 annually. With Metromile she pays a $40 monthly base rate plus 6 cents per mile. She drives about 4,000 miles annually. That’s $480 in base payments plus $240 in mileage charges for a total of $720 yearly. She’s saving $680 annually just because she doesn’t drive much anymore.

9. Review and adjust coverage as life changes

Your insurance needs change as your life evolves. Reviewing your policy annually and adjusting coverage accordingly prevents overpaying.

When you pay off your car loan you can drop collision and comprehensive if the math supports it. When you move to a safer neighborhood you might reduce certain coverages. When your teen driver moves out you remove them from your policy and watch your premium drop by thousands.

Life events that impact your insurance costs:

- Getting marriedSave $160/year

- Paying off car loanSave $600/year

- Teen driver moves outSave $2,800/year

- Urban to suburban moveSave $450/year

- Retirement (senior discounts)Save $200/year

- Buying a home (bundling)Save $400/year

Adding a spouse to your policy often reduces rates. Married drivers typically pay less than single drivers because statistics show they file fewer claims. When I got married my individual premium was $1,650 and my wife’s was $1,450. Combined on one policy we pay $2,400 total instead of $3,100. That’s $700 in annual savings just from the multi-driver and married discounts.

Moving to a lower-risk ZIP code can dramatically reduce your premium. If you relocate notify your insurer immediately and don’t wait until renewal. I moved from a city neighborhood to a suburban area and my premium dropped by $340 annually because the new ZIP code has lower theft and accident rates.

Set a calendar reminder each year to review your policy and life circumstances. Five minutes of review can identify savings opportunities you’d otherwise miss.

Group together small changes for big savings

Each individual strategy might save 5% or 10% but stacking multiple tactics creates substantial savings. Bundle your policies for 20% off. Raise your deductibles for another 15%. Add usage-based monitoring for 25% more. Claim safe driver, low mileage, and automatic payment discounts. Suddenly you’re paying 50% to 60% less than before.

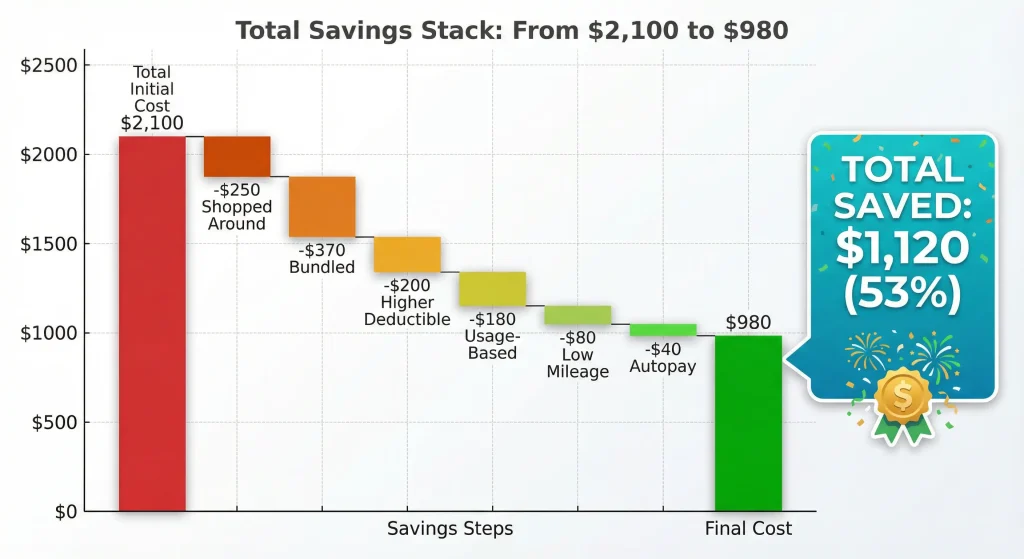

My complete savings breakdown:

Total savings from $2,100 to $980 is $1,120 annually. That’s 53% off my original premium. Same coverage, same protection, just smarter about how I’m buying it. Over five years that’s $5,600 back in my pocket.

Most of these strategies don’t sacrifice protection. You’re simply being smarter about what you pay for coverage that actually protects you. Understanding exactly what different types of coverage provide and whether you need them is the first step toward intelligent insurance decisions that save money without leaving you exposed.

The insurance companies aren’t going to volunteer these savings. You have to ask for them, shop around for them, and actively manage your policy. But the payoff is worth every minute of effort.

Stay covered, stay safe, and happy driving.