Down payment guide: how much to put down on a used car

The standard recommendation suggests putting 20% down on a used vehicle to avoid negative equity and secure favorable loan terms. However, your optimal down payment depends on the car’s price, your credit score, available savings, and monthly budget constraints. Larger down payments reduce interest costs, lower monthly obligations, and improve approval odds with lenders. Conversely, minimal down payments preserve cash reserves for emergencies and maintenance. Balancing these factors requires understanding the full spectrum of used car financing mechanics and calculating your total cost of ownership beyond just the purchase price.

The 20% rule and why it exists

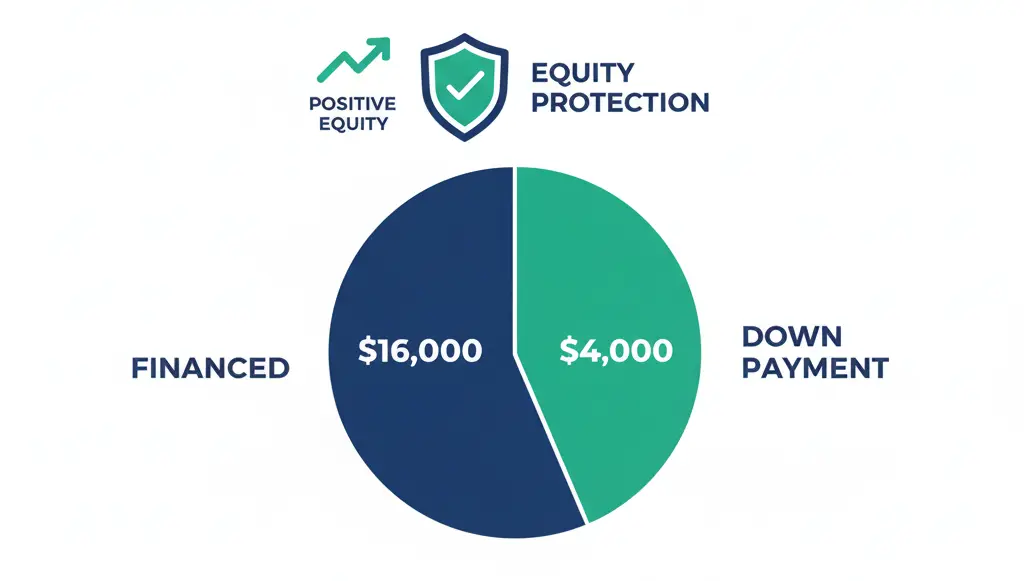

Financial advisors commonly recommend 20% down for used cars as a general guideline. This percentage creates immediate equity in the vehicle since used cars depreciate slower than new ones. Starting with equity protects you from owing more than the car is worth if you need to sell or trade it early.

A $20,000 used car with a $4,000 down payment leaves you financing $16,000. The car might depreciate to $17,000 after one year meaning you have positive equity even after depreciation. Without that down payment, you’d owe more than the car’s value creating an underwater loan situation.

Lenders favor 20% down payments because they reduce default risk. You have skin in the game which makes you less likely to walk away from the loan if financial troubles hit. This reduced risk often translates to lower interest rates saving you money over the loan term.

The 20% guideline isn’t absolute though. Your circumstances might justify more or less depending on factors like your credit score, the vehicle’s age, and your emergency fund status. Treating it as a starting point for calculations makes more sense than viewing it as a strict requirement.

How down payments affect interest rates

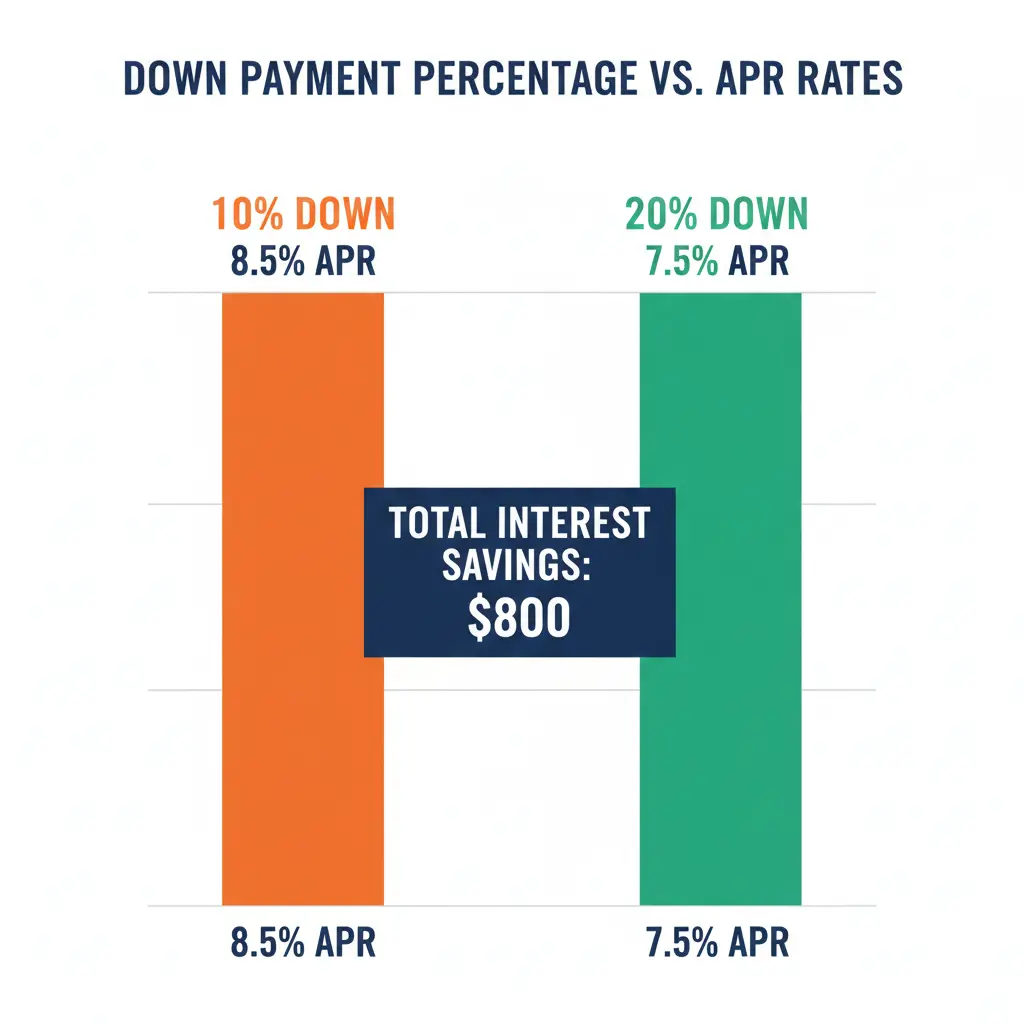

Putting more money down directly impacts the APR lenders offer. A borrower with a 680 credit score might receive 8.5% APR with 10% down but 7.5% APR with 20% down. That single percentage point saves roughly $800 in interest on a $20,000 loan over 60 months.

The relationship between down payment and rate isn’t always linear. Jumping from 5% to 10% down might not change your rate but moving from 10% to 20% could drop it significantly. Lenders have internal thresholds where risk assessments change triggering better pricing.

Credit score interacts with down payment size to determine your final rate. Someone with a 750 score putting 10% down might get the same rate as a 650 score borrower putting 25% down. The stronger your credit, the less you need to compensate with a large down payment.

Older vehicles often require larger down payments to qualify for reasonable rates. A 10-year-old car might need 25% to 30% down where a three-year-old vehicle only needs 15%. Lenders view older cars as higher risk due to potential mechanical issues and faster depreciation.

Calculating what you can afford

Start with your total savings and subtract three to six months of living expenses for emergencies. The remaining amount represents your maximum available down payment. Never drain your emergency fund completely to maximize your down payment because unexpected expenses will arise.

Consider upcoming maintenance and repair costs when determining down payment size. Used cars need immediate attention items like tires, brakes, or timing belts. Setting aside $1,000 to $2,000 for first-year maintenance prevents you from going into debt for necessary repairs.

Calculate your target monthly payment based on your budget before deciding on down payment amount. If you can afford $400 monthly, work backwards using loan calculators to find the right balance between purchase price, down payment, and loan term. Sometimes a smaller down payment with a less expensive car makes more sense than stretching your budget.

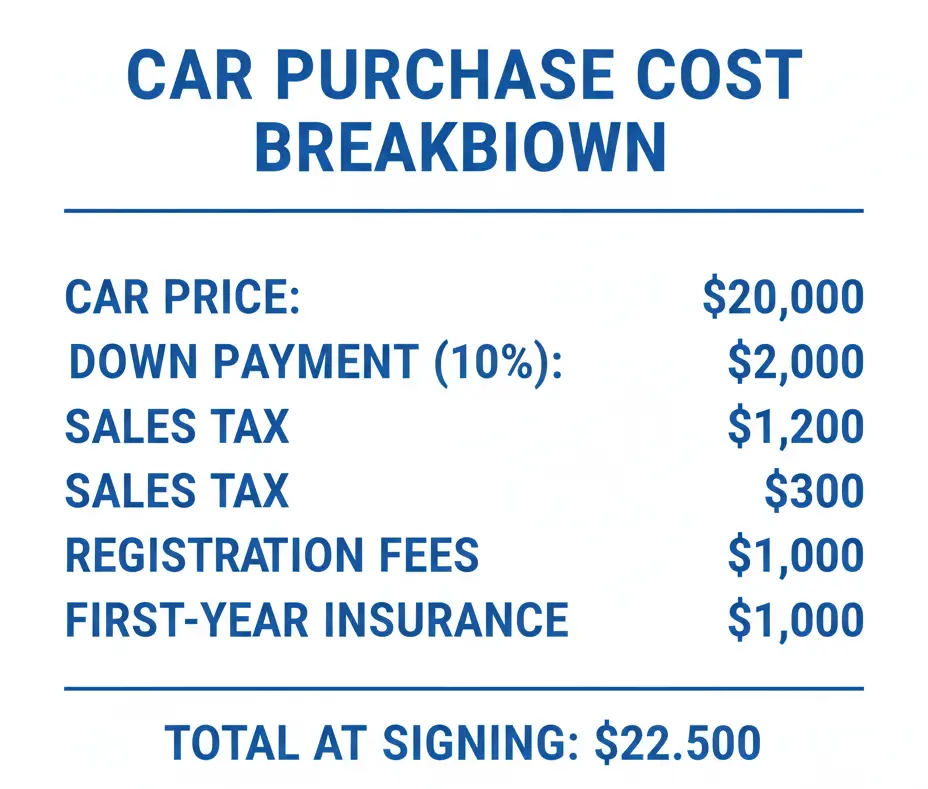

Account for other purchase costs beyond the down payment. Sales tax, registration, title fees, and initial insurance payments add thousands to your upfront costs. A $20,000 car might require $22,500 total at signing when including these expenses plus a 10% down payment.

Minimum down payment requirements by lender type

Banks typically require 10% to 20% down on used car loans. They enforce higher minimums for subprime borrowers or older vehicles. Someone with excellent credit buying a two-year-old car might get approved with 10% down while a borrower with a 600 credit score needs 20% or more.

Credit unions often accept lower down payments than banks because of their member-focused mission. Some credit union programs approve loans with as little as 5% down for members in good standing. This flexibility helps buyers who lack substantial savings but have stable income.

Online lenders vary widely in their down payment requirements. Some approve zero-down financing for prime borrowers while others mandate 15% regardless of credit score. Their automated underwriting systems use algorithms that weigh multiple factors beyond just down payment percentage.

Subprime lenders serving buyers with challenged credit routinely require 20% to 30% down. The large down payment compensates for elevated default risk and ensures they can recover their money through repossession if necessary. Buy-here-pay-here dealers might accept less down but charge interest rates that make the total cost prohibitive.

Strategic down payment approaches

Putting exactly 20% down works for many buyers but consider adjusting based on your situation. If increasing to 25% drops your interest rate by a full percentage point, the extra 5% investment pays for itself through interest savings. Run the numbers to find the optimal amount.

Sometimes making a smaller down payment preserves cash for other investments or debt payoff. If you’re carrying credit card debt at 18% APR, paying down that balance generates better returns than putting extra money toward a car down payment. Prioritize high-interest debt before maximizing auto down payments.

Trade-in equity counts toward your down payment reducing the cash needed upfront. A trade worth $5,000 on a $20,000 purchase means you only need $1,000 additional cash to reach 20% down plus sales tax. Negotiate the trade-in value separately from the purchase price to maximize this benefit.

Saving for a larger down payment might cost you more if car prices are rising faster than you can save. Regional markets experiencing rapid price increases sometimes reward buyers who jump in with smaller down payments rather than waiting. Balance the savings rate against market trends in your area.

Impact on monthly payments and loan terms

Down payment size directly affects your monthly obligation. On a $20,000 car at 7% APR for 60 months, a 10% down payment yields $355 monthly payments. Increasing to 20% down drops payments to $316 saving you $39 monthly or $2,340 over the loan term.

The payment reduction creates breathing room in your budget for other expenses or unexpected costs. That extra $39 monthly funds your insurance increase, covers additional fuel costs, or builds an emergency fund. Small monthly differences compound into meaningful flexibility over time.

Larger down payments enable shorter loan terms without inflating monthly payments. You might finance $16,000 over 48 months for the same monthly payment as $18,000 over 60 months. The shorter term saves substantial interest and gets you to debt-free ownership faster.

Some buyers intentionally choose smaller down payments with longer terms to keep payments low during the early years. They plan to make extra principal payments later when their financial situation improves. This approach requires discipline to follow through on the extra payment strategy.

When less down makes sense

Preserving cash for a house down payment trumps maximizing your car down payment. If you’re saving for a home and need transportation now, putting the minimum down on a car keeps your housing fund intact. Real estate offers better long-term appreciation than vehicles.

Business owners and self-employed individuals benefit from keeping cash accessible for operating expenses or opportunities. Tying up capital in a depreciating asset like a car reduces business flexibility. They might choose minimal down payments even if they could afford more.

Zero percent or low promotional financing sometimes comes with down payment requirements or restrictions. Dealers offering special rates might incentivize smaller down payments to move inventory. Calculate whether the promotional rate saves more than making a large down payment at a standard rate.

Emergency fund gaps justify smaller down payments too. If you have less than three months of expenses saved, building that reserve takes priority over a large car down payment. Drive something less expensive or put down less to maintain financial stability.

Down payment sources beyond savings

Trading in your current vehicle provides instant down payment funds without touching savings. Get multiple offers from online buyers like Carvana, Vroom, and local dealers to maximize trade value. Sometimes private party sales yield more money but require extra time and effort.

Selling items you no longer need generates down payment cash quickly. Electronics, furniture, collectibles, or hobby equipment gathering dust converts to useful transportation funds. Online marketplaces make selling easier than ever.

Side gig income dedicated to a car fund builds down payments without impacting your regular budget. Driving for rideshare services, freelancing, or part-time work adds hundreds monthly. Three to six months of side income can fund a substantial down payment.

Family gifts or loans offer another option if you have supportive relatives. Formalize any loan agreements in writing to preserve relationships and clarify expectations. Some lenders count gift funds toward down payments if properly documented.

Avoiding negative equity situations

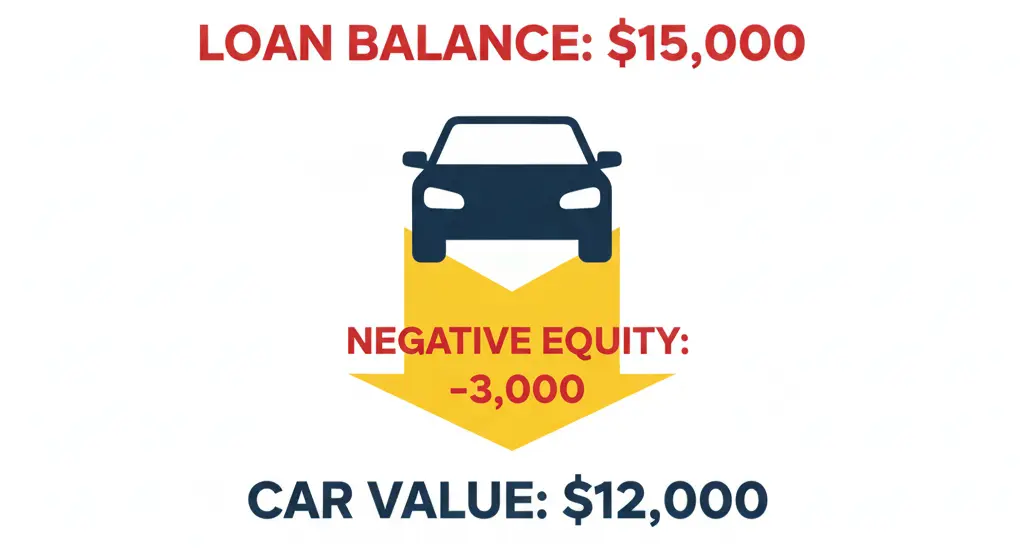

Negative equity happens when you owe more than the car is worth. Small down payments combined with long loan terms create this situation because depreciation outpaces principal paydown. Owing $15,000 on a car worth $12,000 traps you in the loan until you pay it down.

Gap insurance protects against negative equity if the car is totaled or stolen. Your regular insurance pays the car’s actual value but gap insurance covers the difference between that value and your loan balance. This coverage costs $300 to $500 as a one-time fee through credit unions or about $20 monthly through dealers.

Rolling negative equity from a previous car into a new loan creates compounding problems. You’re financing your old debt plus the new vehicle putting you underwater immediately. Break this cycle by driving your current car longer while paying down the loan or accepting a smaller down payment on the next purchase.

Larger down payments prevent negative equity from developing. Starting with 20% equity gives you a buffer against normal depreciation. Even if the car loses 15% of its value in year one, you maintain positive equity throughout the loan.

Choosing the right down payment amount balances your immediate cash position against long-term interest costs and loan flexibility. Most buyers benefit from targeting 15% to 20% down as a sweet spot between manageable cash outlay and favorable loan terms. Once you’ve determined your down payment strategy, comparing lenders who specialize in used car financing helps you secure the best overall deal combining competitive rates with terms that match your financial situation.