Compare Car Insurance Quotes: Complete Shopping Guide

Getting cheap car insurance quotes is easy, but getting accurate, comparable quotes requires strategy. Most shoppers make critical errors like comparing different coverage levels or overlooking company financial ratings, leading to either overpaying or choosing unreliable insurers. The key is requesting identical coverage from multiple companies, evaluating their claims handling reputation, understanding each insurer’s specialties, and looking beyond the sticker price to assess true value.

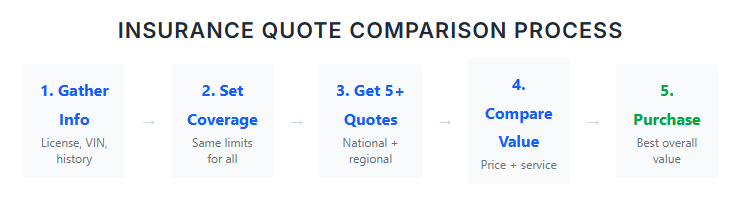

Gather your information before requesting quotes

Jumping into quote requests without preparation wastes time and produces inaccurate results. Insurance companies need specific information to calculate accurate premiums.

Information Checklist

Having all this information ready lets you provide consistent details to every company. Inconsistent information produces quotes that aren’t truly comparable.

Request identical coverage from every insurer

This is where most people mess up. They get quotes with different coverage levels and then wonder why prices vary so much.

Warning: Small differences create huge price variations. A quote with $500 deductibles will obviously cost more than one with $1,000 deductibles. That doesn’t mean the company is more expensive it means you requested different coverage.

Write down your exact specifications: liability limits, collision deductible, comprehensive deductible, medical payments or PIP amount, uninsured motorist limits, and any additional coverages like rental reimbursement or roadside assistance.

Pay attention to policy periods. Some companies quote six-month policies while others quote annual policies. Make sure you’re comparing equivalent time periods.

Look beyond the bottom-line price

The cheapest policy isn’t automatically the best policy. Price matters but it’s not the only consideration.

- Check Financial Strength: AM Best rates insurance companies on their ability to pay claims. You want a company rated A- or better.

- Research Satisfaction: JD Power publishes annual rankings based on customer satisfaction. Consumer Reports also rates insurance companies.

- Look at Complaints: State insurance departments track complaints. The NAIC publishes complaint ratio data for each company.

- Evaluate Digital Tools: Can you file claims through a mobile app? Is policy management available online? Modern technology matters.

| Company | Best For | Avg. Premium | AM Best | Key Discount |

|---|---|---|---|---|

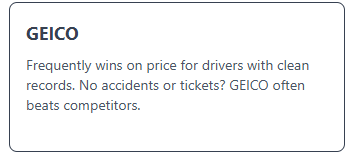

| GEICO | Clean driving records | $1,245/yr | A++ | Multi-vehicle 25% |

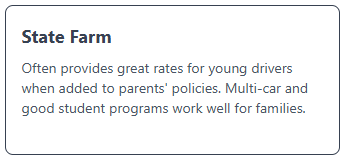

| State Farm | Families & young drivers | $1,428/yr | A++ | Good student 20% |

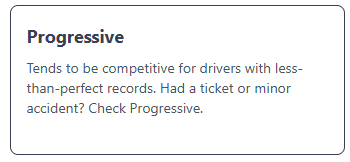

| Progressive | Less-than-perfect records | $1,356/yr | A+ | Snapshot up to 30% |

| Allstate | Tech-savvy drivers | $1,589/yr | A+ | Drivewise up to 40% |

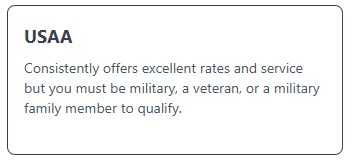

| USAA | Military families | $1,098/yr | A++ | Military 15% |

| Liberty Mutual | Customizable coverage | $1,467/yr | A | Bundle up to 29% |

* Average premiums based on national data for 35-year-old drivers with clean records. Individual rates may vary.

Understand claims handling reputation

Claims handling matters more than anything else when you actually need your insurance. A company that’s difficult to work with after an accident isn’t worth savings on your premium.

Questions to Ask About Claims

- Do they use in-network repair shops or allow you to choose your own?

- How quickly do they respond to claims? What’s the average time from claim to payment?

- Do they offer rental car coverage directly or through reimbursement?

- Do they have local adjusters in your area?

Recognize that different companies excel with different customers

Insurance companies don’t all compete for the same customers. Each has preferred customer profiles where they offer the best rates.

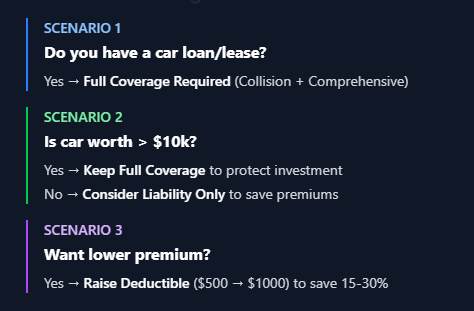

Coverage Decision Tree

Get quotes from the right mix of companies

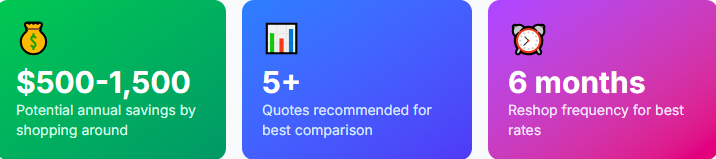

Cast a wide net but focus your energy appropriately. Getting 20 quotes provides diminishing returns compared to five or six well-chosen options.

Instead of casting a wide net randomly, focus your energy on a mix of insurers. You’ll want to get quotes from two or three major national brands like GEICO or State Farm, but don’t stop there. Include one or two regional companies like Erie or Auto-Owners if they operate in your area, as they often have competitive rates. It’s also worth checking with any affinity groups you belong to alumni associations or professional organizations often have negotiated discounts. Finally, consider asking an independent agent to shop your information across multiple carriers for you.

Ask the right questions before committing

When you narrow down to your top choices, dig deeper with specific questions.

- Rate Guarantee: Ask about their rate guarantee period. Some companies guarantee rates for six months or a year.

- Renewal History: Find out about renewal rate history. Some offer low intro rates then increase significantly.

- Accident Forgiveness: Inquire about accident forgiveness programs is it standard or an extra charge?

- Payment Options: Clarify payment options and fees. Paying annually usually saves money vs. monthly.

Watch for red flags during the quote process

Watch out for red flags when you’re shopping around. If one company quotes you 50% less than everyone else for identical coverage, something’s off. Either they missed coverage you requested, or the quote has errors. I’ve seen this happen too many times.

Same thing with pushy sales tactics. Companies that pressure you hard or make getting a quote unnecessarily complicated? That’s a preview of how they’ll handle your claim. If it’s this hard to give them money now, imagine trying to get money back from them after an accident.

Check their reputation before signing anything. Look for patterns in reviews. One or two complaints mean nothing but consistent problems with state insurance departments tell you everything you need to know.

Pricing varies wildly between companies even for identical drivers. USAA typically offers the best rates around $1,100 annually but you need military ties to qualify. Can’t get USAA? Progressive and GEICO usually come in next, somewhere between $1,200 and $1,350.

State Farm and Liberty Mutual tend to run higher, often $1,400 to $1,500. Allstate typically sits at the expensive end, averaging over $1,500. These are just ballpark figures though. Your actual rate depends entirely on your specific situation.

Make your final decision based on value, not just price

After gathering quotes and researching companies, evaluate the total package rather than just comparing premiums.

Value Assessment Checklist

- ✓Does the quote include everything you need?

- ✓Are the limits adequate for your situation?

- ✓Strong financial ratings (A- or better)?

- ✓Positive customer reviews for claims?

- ✓Mobile app and online management?

- ✓Future discount opportunities?

Sometimes paying $50 more annually for dramatically better service and stronger financial stability makes sense. Other times the cheapest option provides everything you need. The right choice depends on your specific situation and priorities.

Key Takeaways

- Always get at least 5 quotes with identical coverage for accurate comparison

- Check financial ratings and customer reviews, not just price

- Different insurers excel with different customer types shop strategically

- Reshop every 6 months loyalty rarely pays in insurance

Stay covered, stay safe, and happy driving.