Car insurance minimums by state: the stuff nobody tells You

Because meeting the legal minimum and being properly protected are two very different things.

Here’s the thing about car insurance laws in America they’re a mess. Forty-nine states demand you carry coverage (New Hampshire being the rebel holdout), but what they actually require? It’s all over the map.

California says 15/30/5 is enough. Michigan? They went with unlimited PIP for years. And that spread tells you something important: these minimums are about legal compliance, not real-world protection.

Most of these laws were written when a hospital stay cost what a nice dinner does now. Medical expenses have skyrocketed. Car prices have exploded. But the insurance minimums? Many haven’t budged since your parents were learning to drive

This knowledge becomes critical when building a comprehensive auto insurance strategy that actually safeguards your assets.

The bottom line: Understanding your state’s specific rules and why they probably aren’t enough could save you from financial disaster down the road.

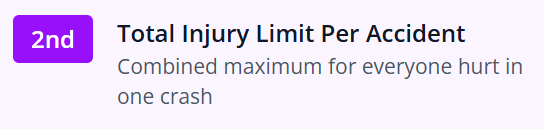

What those three numbers really mean

You’ve probably seen insurance requirements written like “25/50/25” and wondered what that cryptic string actually means. Let me break it down in plain English.

So, when California requires 15/30/5, they’re saying: $15,000 per injured person, $30,000 total for injuries per accident, and $5,000 for property damage.

Reality check

A single night in the ER can blow past $15,000. A new Honda Accord runs about $28,000. California’s $5,000 property damage limit won’t even cover the bumper on some SUVs. If your insurance runs out, guess who’s paying the rest? You. Out of your bank accounts, your wages, potentially your house.

Comprehending these three figures is only the beginning. These state minimums cover liability coverage, but it’s only one aspect of the picture. Additionally, you need to think about gap, PIP, collision, and comprehensive insurance. You are protected in different ways by each one, and if you skip one, you may be exposed in unexpected ways. Before determining how much to carry, it’s helpful to know what each type of auto insurance coverage actually protects if you’re creating a policy from scratch.

Why are these minimums still so ridiculously low?

I get asked this constantly, and honestly? It’s a mix of bureaucratic inertia, political cowardice, and good old-fashioned lobbying.

Most state insurance laws were hammered out in the ’70s and ’80s. Back then, these numbers actually meant something. A hospital stay didn’t require a second mortgage. A new car cost what we now spend on a decent used one.

“Updating these laws requires legislators to vote for something that will raise insurance costs. That’s political poison, even when it’s the right thing to do.”

Some states have tried. Maine bumped their requirements. A handful of others made modest tweaks. But meaningful reform? Rare. Politicians know that “I raised your insurance rates” doesn’t look great on a campaign flyer even if “I protected you from bankruptcy” would be the honest framing.

And then there’s the insurance industry itself, which sends mixed signals. Sometimes they fight higher minimums (complicates their pricing models). Sometimes they support increases (higher coverage = higher premiums = more revenue). It’s complicated, and meanwhile, drivers like you and me are stuck with outdated protections.

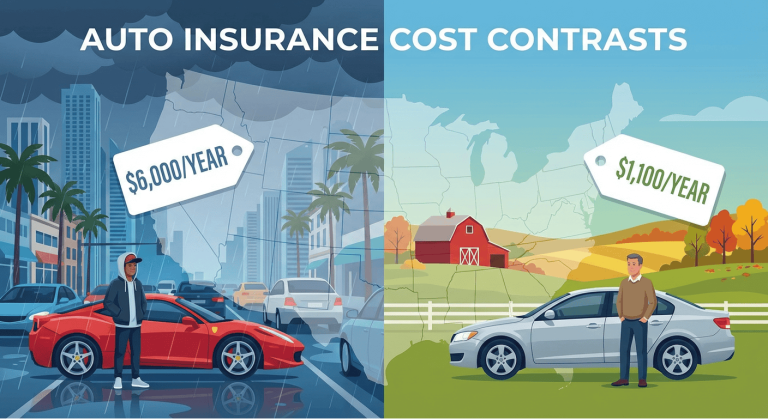

State-by-state: where does yours stack up

I’ve spent way too many hours digging through state insurance codes. Here’s the short version of what I found:

| State | Minimum Required Coverage | Coverage Level |

|---|---|---|

| Alaska | 50/100/25 | Above Average |

| Maine | 50/100/25 | Above Average |

| Texas | 30/60/25 | Mid-Range |

| Minnesota | 30/60/10 | Mid-Range |

| Arizona | 25/50/15 | Mid-Range |

| Nevada | 25/50/20 | Mid-Range |

| Georgia | 25/50/25 | Mid-Range |

| California | 15/30/5 | Very Low |

| Florida | PIP Only* | No BI Required |

| New Hampshire | None Required | No Mandate |

*Florida requires $10,000 PIP but no bodily injury liability coverage. Yes, really.

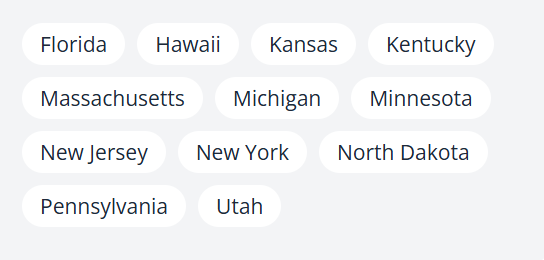

No fault states: a different beast entirely

About a dozen states do things differently with what’s called “no-fault” insurance. The list includes Florida, Michigan, New York, New Jersey, and a handful of others.

The concept sounds nice on paper: after an accident, your own insurance pays your medical bills regardless of who screwed up. No waiting around while insurers argue about fault. No delays in getting treatment covered.

No-Fault States at a Glance

The catch? You generally can’t sue the other driver unless your injuries hit certain thresholds a specific dollar amount, permanent damage, or particular injury types like broken bones.

Michigan’s situation deserves special mention. They required unlimited lifetime medical coverage for years. Sounds great until you see the premiums consistently the highest in the nation by a mile. Recent reforms now let drivers pick lower PIP limits if they’ve got health insurance that covers accidents. Rates are coming down, but Michigan’s still expensive.

Florida? They mandate $10,000 in PIP coverage but don’t require any bodily injury liability. You might have coverage for yourself but nothing if you hurt someone else. It’s a bizarre setup that leaves everyone more exposed.

At-fault states: the traditional approach

Most states still use the traditional “at-fault” system. It’s simpler to understand whoever caused the accident, their insurance pays for the damage.

The downside is figuring out fault takes time. Insurance companies argue. Witnesses disagree. Police reports might be unclear. All while you’re waiting to get your car fixed or your medical bills paid.

In these states, uninsured motorist coverage isn’t just nice to have it’s essential. If someone without insurance rams into you, UM coverage picks up the slack. Without it, your only option is suing someone who probably doesn’t have the money to pay anyway.

Pro Tip

Kentucky, New Jersey, and Pennsylvania let you choose between systems. “Limited tort” saves money but restricts your right to sue. “Full tort” costs more but preserves your legal options. Most experts myself included recommend full tort if your budget allows. The savings aren’t worth giving up your rights after a serious injury.

Another important point regarding at-fault states is that, in the event of an accident, understanding the claims procedure can save you thousands of dollars and weeks of headaches. The actions you take at the scene, such as recording damage, gathering witness information, and corresponding with adjusters, have a direct impact on how quickly your claim is settled. I’ve witnessed people lose money just because they were unsure of what to do during the first twenty-four hours. The kind of preparation that pays off when it matters most is knowing exactly how to successfully file an auto insurance claim before you ever need it.

What Happens If You Get Caught Without Insurance

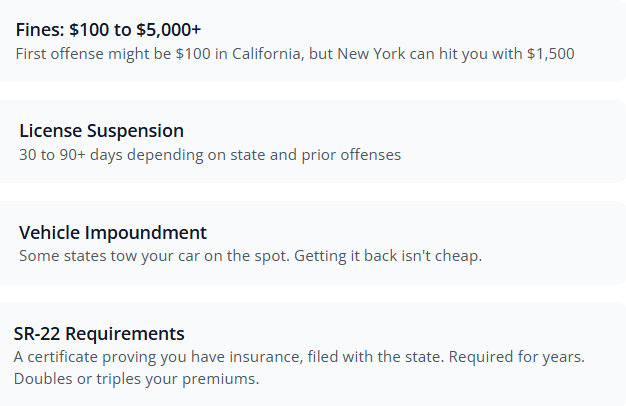

Short answer: nothing good. Every state takes this seriously, though the specific punishments vary.

But here’s the real kicker: legal penalties are the least of your worries. Cause an accident without insurance and you’re personally on the hook for everything. Medical bills. Lost wages. Pain and suffering. We’re talking potential bankruptcy over a single mistake.

Why you should carry more than the minimum (and It’s Cheaper Than You Think

I’m going to be blunt: if you’re carrying only state minimum coverage, you’re taking a massive gamble with your financial future.

Consider what $15,000 in bodily injury coverage actually gets you in 2025. A serious injury requiring surgery and rehab? That’s easily $100,000 or more. Ongoing care for permanent disabilities? We’re talking seven figures. Your minimum coverage runs out before the ambulance reaches the hospital.

What experts actually recommend

“But that must cost a fortune,” I hear you saying. Actually? Not really.

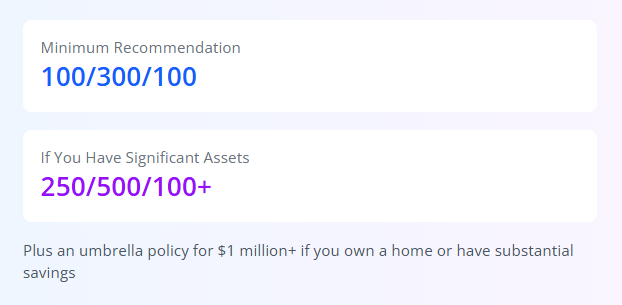

Going from 25/50/25 to 100/300/100 typically adds somewhere between $200 and $400 to your annual premium. That works out to maybe $20-35 a month for dramatically better protection. An umbrella policy adding another million in coverage might cost $150-300 per year.

Compare that to the alternative: losing your house, having your wages garnished, watching your retirement savings evaporate all because you saved a few bucks on insurance.

A word for high-risk drivers

If you’ve got a DUI on your record, multiple accidents, or serious moving violations, you’re in a different situation entirely.

Most states will require an SR-22 certificate proof of insurance filed directly with the DMV. Your insurance company has to notify the state if your coverage lapses, and you’ll carry this requirement for three to five years typically.

The bad news: expect to pay double or triple your previous rates. Not every company offers SR-22 policies, so your options are limited. Shop around anyway the price differences can be substantial.

Florida and Virginia take it further with FR-44 certificates for DUI offenses. These require even higher liability limits usually 100/300/50 on top of the higher premiums.

The Bottom Line

State minimum insurance requirements exist to keep you legal, not to keep you protected. There’s a big difference.

Determine your coverage based on what you actually have to lose your home, your savings, your future income rather than what some law written in 1978 says is “enough.”

Factor in how many uninsured drivers share the roads in your state. Some areas have rates over 20%. Uninsured motorist coverage isn’t optional in those places it’s survival.

And here’s the thing most people miss that extra cost often shrinks even further when you know where to look. Bundling discounts, safe driver programs, raising your deductibles strategically there are real ways to lower your auto insurance premium without sacrificing the coverage you actually need. The savings from one or two discounts can easily offset the cost of better liability limits

And remember: the cost difference between bare-bones coverage and real protection is usually a lot smaller than people assume. A few hundred dollars a year is nothing compared to what’s at stake.

Stay covered, stay safe, and happy driving.