Can switching auto insurance lower your rate after an accident in California?

After an accident, many drivers assume their auto insurance costs are locked in for years. A rate increase arrives at renewal, frustration sets in, and the common belief is that switching insurers will not help. In California, this assumption is often wrong.

California’s insurance regulations, fault rules, and rating timelines create situations where switching auto insurance after an accident can reduce premiums, sometimes substantially. The key lies in understanding how accidents are classified, how long they affect pricing, how different insurers weigh claims, and most importantly when switching makes sense.

This article explains whether switching auto insurance can lower your rate after an accident in California, how insurers evaluate accident history, what timing strategies work best, and which mistakes drivers should avoid. It is written for drivers seeking realistic cost control after a claim and for automotive insurance niche sites building evergreen authority content.

How accidents affect auto insurance rates in California

California insurers do not treat all accidents equally.

Key factors that matter

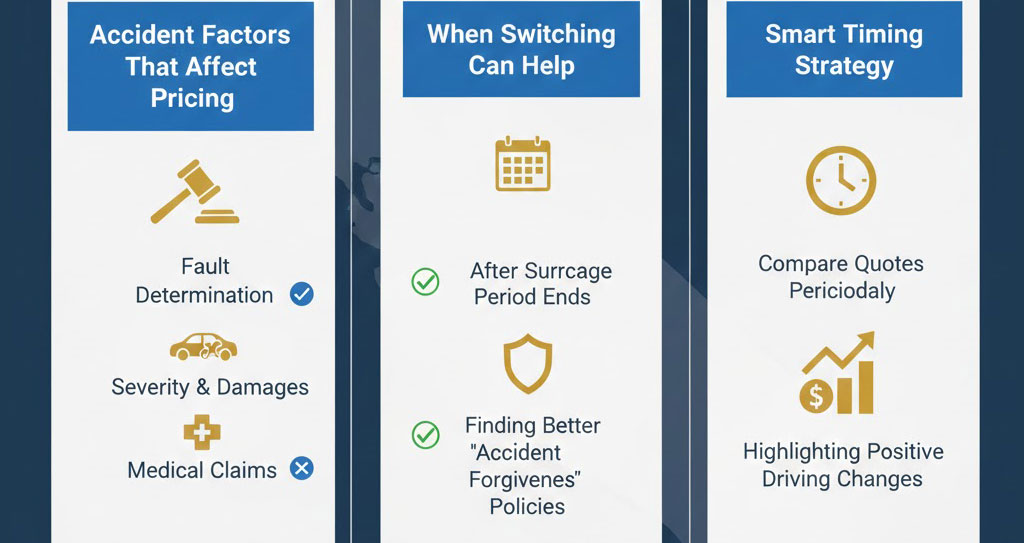

When pricing policies after an accident, insurers evaluate:

- Fault determination

- Type of claim (collision vs. comprehensive)

- Severity of damage

- Presence of bodily injury

- Time elapsed since the accident

Unlike some states, California restricts how insurers can surcharge drivers, making accident impact more nuanced.

Fault vs. not-at-fault accidents

Fault determination is the most important variable.

At-fault accidents

If you are found primarily at fault:

- Premiums typically increase

- Eligibility for certain discounts may be affected

- Surcharges may apply for multiple years

However, the size and duration of the increase vary widely by insurer.

Not-at-fault accidents

If you are not at fault:

- Many insurers apply little or no surcharge

- Some insurers ignore not-at-fault claims entirely

- Pricing impact is often temporary or minimal

Switching insurers after a not-at-fault accident often results in better pricing.

Comprehensive claims vs. collision claims

Not all claims reflect driving behavior.

Comprehensive claims

Examples include:

- Theft

- Vandalism

- Weather damage

- Animal collisions

These claims are typically weighted less heavily because they are not tied to driver negligence. Switching insurers after comprehensive claims frequently produces better results than expected.

Collision claims

Collision claims tied to at-fault accidents usually have a greater pricing impact, but differences in insurer weighting still matter.

How long do accidents affect insurance rates in California?

California insurers generally focus on a three-year rating window.

Practical implications

- Recent accidents matter most

- Older accidents gradually lose impact

- Pricing improves automatically over time

Switching insurers immediately after an accident may not always be optimal but switching after time has passed often is.

Why different insurers price accidents differently

Even under the same laws, insurers interpret risk differently.

Examples of insurer differences

Some insurers:

- Penalize first accidents lightly

- Emphasize frequency over severity

- De-emphasize older claims

Others:

- Apply strict surcharges

- Penalize all at-fault accidents equally

This explains why switching can lower rates even when the accident remains on record.

When switching after an accident makes sense

Switching insurers is most effective after an accident when:

- The accident was not at fault

- The claim was comprehensive rather than collision

- Time has passed since the incident

- A discount eligibility issue has been corrected

- Your mileage or lifestyle has changed

Timing determines success.

When switching after an accident does not help

Switching may offer limited benefit when:

- The accident involved serious bodily injury

- Fault was clearly established

- The accident occurred very recently

- Multiple claims exist within a short period

In these cases, waiting for claims to age can produce better results.

Accident forgiveness and switching insurers

Accident forgiveness programs often cause confusion.

Important reality

- Accident forgiveness is insurer-specific

- It does not transfer when switching

- New insurers still evaluate accident history

However, some insurers price drivers more favorably than others even without forgiveness programs.

Switching after regaining good driver discount eligibility

In California, the Good Driver Discount is mandatory once eligibility is restored.

Why this matters

If an accident caused temporary loss of eligibility:

- Eligibility may return after three years

- Switching insurers at that moment ensures proper application

This timing strategy frequently produces the largest post-accident savings.

Switching after an accident vs. staying put

Staying with the same insurer

Pros:

- Claims familiarity

- Administrative simplicity

Cons:

- Rate increases may persist

- Discount errors may remain

Switching insurers

Pros:

- Fresh underwriting evaluation

- Corrected mileage and discount application

- Potentially lower long-term rates

Cons:

- Requires careful comparison

- Documentation must be accurate

In California’s regulated market, switching often favors informed drivers.

How to compare quotes after an accident

Drivers should:

- Compare at least three insurers

- Match coverage exactly

- Verify discount application

- Ask how claims are weighted

Quote comparison quality matters more than quantity.

Switching with an open or recent claim

California allows switching even with an open claim.

Key rules

- The old insurer handles the existing claim

- The new insurer covers future incidents

- Claims history still follows the driver

Switching should be timed to avoid confusion and misreporting.

Common mistakes drivers make after an accident

- Switching too early without comparison

- Assuming all insurers will price the same

- Ignoring not-at-fault status

- Overestimating mileage

- Canceling coverage incorrectly

These mistakes often erase potential savings.

Strategic waiting: When patience pays off

Sometimes the best move is waiting.

Waiting makes sense when

- An accident is close to aging off

- Eligibility for discounts is about to return

- Mileage reduction is not yet reflected

Switching too early can lock in higher pricing unnecessarily.

An accident does not permanently trap California drivers into high insurance rates. Because of strict regulations, limited surcharge windows, and insurer-specific pricing models, switching auto insurance after an accident can lower premiums in many situations.

The key is understanding fault, timing the switch strategically, and comparing insurers that weigh claims differently. Drivers who approach switching with patience and knowledge often regain control of their insurance costs sooner than expected.

In California, an accident changes the insurance equation but it does not end the opportunity to save.