Bad credit used car financing: options and tips

A credit score below 580 doesn’t eliminate your financing options, though it does require strategic planning. Subprime lenders, buy-here-pay-here dealerships, and credit union special programs cater specifically to borrowers with challenged credit histories. Expect higher interest rates, larger down payment requirements, and shorter loan terms. However, successful repayment rebuilds your credit profile for future purchases. Before committing to any agreement, review the comprehensive landscape of used car financing alternatives to ensure you’re selecting the most favorable terms available for your situation.

Understanding bad credit auto lending

Bad credit generally refers to FICO scores below 580 though some lenders extend the definition to scores below 620. These scores result from late payments, high credit utilization, collections, bankruptcies, or foreclosures. Each negative mark tells lenders you represent higher default risk.

Traditional lenders often reject applications from borrowers with scores below 600. They prefer safer bets where they’re confident in getting repaid. This leaves a substantial market of buyers who need transportation but lack access to mainstream financing.

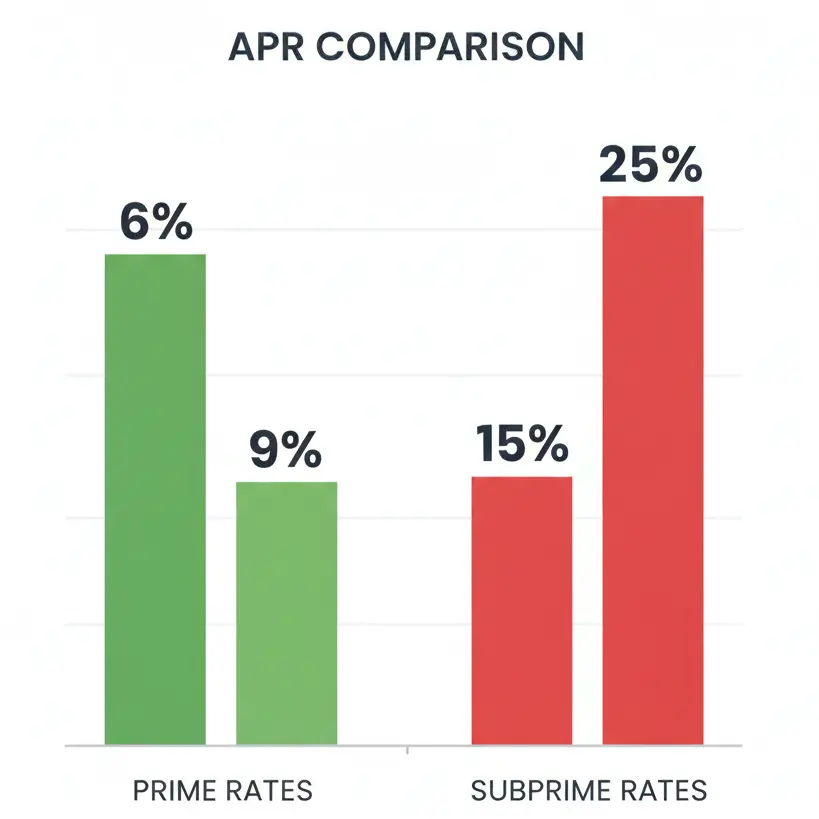

Subprime lenders fill this gap by accepting higher risk in exchange for higher returns. They charge APRs that can reach 15% to 25% compared to the 6% to 9% rates excellent credit borrowers receive. While these rates seem steep, they provide access to financing that otherwise wouldn’t exist.

The subprime lending industry has legitimate players alongside predatory operators. Knowing the difference protects you from abusive terms while still getting the car you need. Research lenders thoroughly and understand exactly what you’re signing before committing.

Subprime lenders who work with bad credit

Capital One Auto Navigator accepts borrowers across the credit spectrum including those with scores in the 500s. Their pre-qualification process uses a soft credit pull that doesn’t hurt your score. You receive a certificate showing dealers you’re approved up to a specific amount.

Credit Acceptance Corporation specializes in deep subprime lending and partners with thousands of dealerships nationwide. They work with borrowers who have bankruptcies, repossessions, or limited credit history. Expect APRs between 15% and 24% depending on your specific situation.

Carvana offers financing for borrowers with credit scores as low as 550. Their online application process provides instant decisions and they deliver the car to your home. However, their rates for subprime borrowers can exceed 20% so compare carefully against other options.Consumer Portfolio Services focuses exclusively on subprime auto lending. They consider factors beyond just credit scores including income stability and down payment amount. This holistic approach sometimes results in approval when other lenders decline.

Buy here pay here dealerships

BHPH lots provide both the vehicle and financing in one location. You make payments directly to the dealer rather than a bank or finance company. This structure eliminates the need for traditional credit approval.

These dealerships accept nearly anyone with steady income and a down payment. They don’t report to credit bureaus in many cases which means successful payments won’t improve your score. The lack of credit reporting cuts both ways though because they also won’t ding your credit if you struggle.

Interest rates at BHPH dealers often reach 20% to 30% with some charging even more. They justify these rates by accepting the highest risk borrowers who have no other options. The vehicles available are usually older with higher mileage and they often cost more than similar cars at traditional dealers.

Weekly or bi-weekly payment schedules are common at BHPH lots. This arrangement helps dealers monitor your payment behavior more closely and reduces their risk. Missing even one payment can trigger repossession because they typically include aggressive repo clauses in contracts.

Do your research before using a BHPH dealer. Check online reviews and Better Business Bureau ratings. Inspect the vehicle thoroughly and get an independent mechanic’s opinion before buying. Many BHPH cars are sold as-is without warranties.

Credit union special finance programs

Some credit unions operate second chance auto loan programs for members with impaired credit. These programs consider the full picture including recent efforts to rebuild credit rather than just focusing on your score.

Community Financial Credit Union offers Fresh Start loans for borrowers with past credit issues. They require proof of income, a reasonable down payment, and evidence you’re working to improve your financial situation. Rates run higher than prime loans but typically stay below 15% APR.

Local credit unions sometimes have more flexibility than national institutions. They can make exceptions for members they know personally or who have other accounts in good standing. Building a relationship by opening a checking account and setting up direct deposit can help when you apply for a car loan.

Credit union auto loans report to credit bureaus so making on-time payments actively rebuilds your credit. This advantage alone makes them preferable to BHPH dealers for borrowers who want to improve their scores.

Strategies to improve approval odds

Saving a larger down payment dramatically increases your chances of approval. Most subprime lenders require at least 10% down but putting down 15% to 20% unlocks better terms. The down payment reduces the lender’s risk by creating instant equity.

Bringing a cosigner with good credit essentially lets you borrow against their creditworthiness. The cosigner becomes equally responsible for the debt which means late payments hurt both of your credit scores. Only ask someone who trusts you completely and understands the risks they’re taking.

Choosing less expensive vehicles improves approval odds because lenders see smaller loans as less risky. A $12,000 car is easier to finance with bad credit than a $25,000 vehicle. Consider reliable used models known for longevity rather than stretching for something newer or flashier.

Proof of stable income matters more with bad credit. Bring recent pay stubs, bank statements, and tax returns showing consistent earnings. Self-employed borrowers should prepare extra documentation proving reliable income streams.

Avoiding predatory lending traps

Yo-yo financing or spot delivery scams let you drive off with the car before financing is truly approved. Days later the dealer calls claiming your loan fell through and pressures you into worse terms. Insist on confirmed financing before taking possession.

Exorbitant fees hidden in the contract inflate your total cost without adding value. Documentation fees above $500, inflated interest rates beyond what the lender approved, and mandatory add-ons like overpriced warranties all drain your budget. Review every line of the contract and question charges that seem excessive.

GPS tracking devices and starter interrupt systems are common with subprime loans. These devices let lenders disable your car remotely if you miss payments. While they serve a legitimate purpose for high-risk lending, ensure you understand the terms around their use.

Extended loan terms of 72 to 84 months might seem attractive because of lower monthly payments. However, you’ll likely owe more than the car is worth for years creating negative equity. Stick to 60 months or less even if it means buying a less expensive vehicle.

Rebuilding credit through car payments

On-time auto loan payments represent one of the fastest ways to improve your credit score. Payment history accounts for 35% of your FICO score so consistently paying on schedule makes a substantial impact.

Set up automatic payments to ensure you never miss a due date. Even one late payment can set back your rebuilding efforts significantly. Most lenders offer autopay with a small rate discount as incentive.

Paying extra toward principal when possible shortens the loan term and reduces interest costs. However, verify your lender applies extra payments to principal rather than advancing the due date. Some subprime lenders structure payments to maximize their interest income.

Consider refinancing after 12 to 18 months of on-time payments. Your credit score should improve enough to qualify for better terms at a traditional lender. Refinancing saves money on interest and demonstrates to future lenders that you’ve successfully managed credit.

Alternative transportation solutions

Sometimes the best decision is waiting a few months while you improve your credit situation. Using public transportation, carpooling, or ride-sharing services might cost less than an expensive subprime loan. The money you save can go toward a larger down payment.

Buying a cheaper car with cash avoids financing altogether. A reliable $5,000 vehicle gets you where you need to go while you rebuild credit. You can always trade up to something nicer once your score improves and you qualify for reasonable rates.

Family loans offer another option if you have relatives willing to help. Put the agreement in writing specifying payment terms and what happens if you can’t pay. Treat it like a real loan to preserve the relationship and prove you’re responsible.

Bad credit auto financing costs more but provides essential transportation while rebuilding your financial foundation. The key is finding legitimate lenders who offer fair terms rather than predatory operators looking to trap you in an endless payment cycle. Once you understand your financing options, comparing lease versus purchase costs helps determine which ownership structure makes more sense for your specific budget and transportation needs.