Average auto insurance costs by state and age in 2026

Alright, so here’s the thing about auto insurance that nobody really tells you straight up: where you live and how old you are basically determining whether you’re paying reasonable rates or getting absolutely gouged.

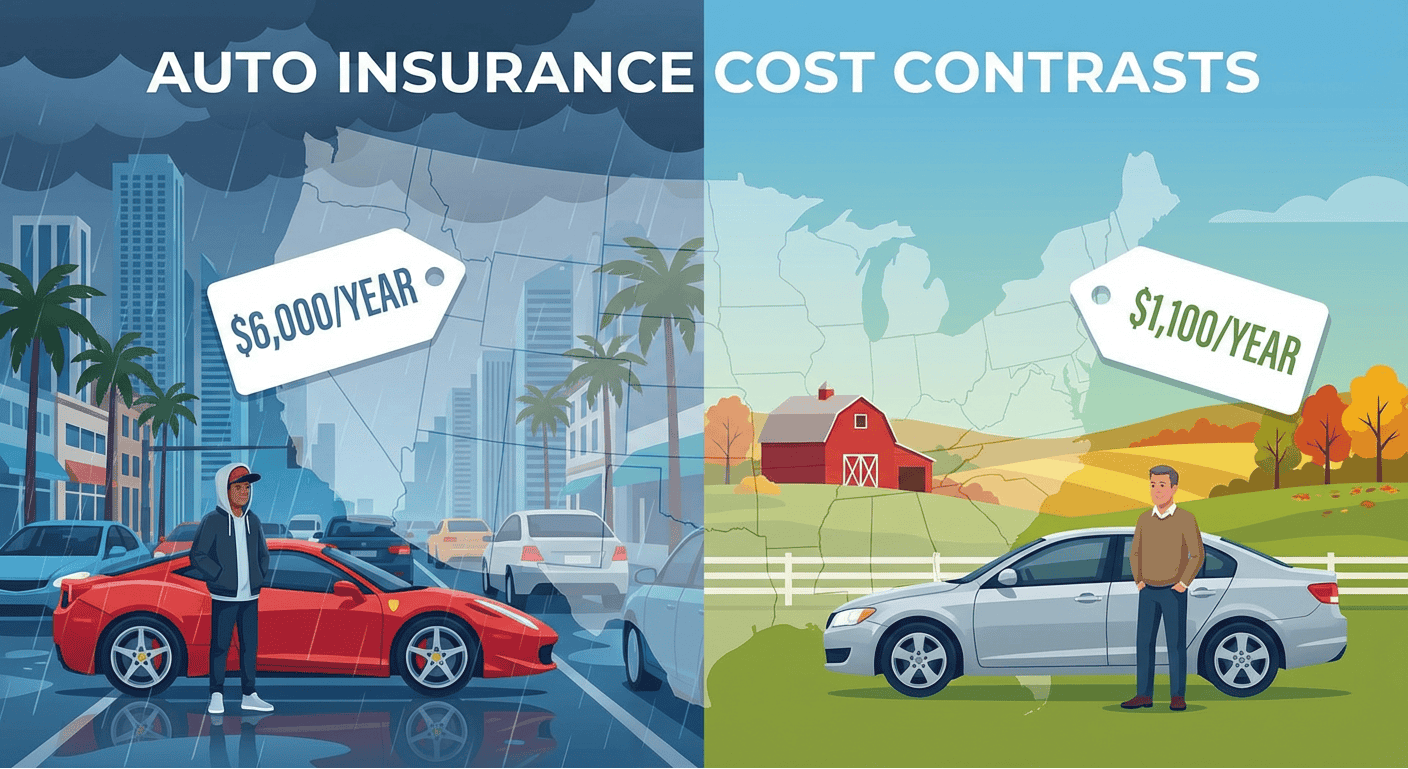

I’ve been writing about this stuff for like ten years now, and I still get shocked sometimes. Last month I was comparing quotes for a friend’s daughter – 18 years old in Michigan – and the cheapest we could find was something insane like $6,200 a year. Meanwhile, my own premium here in Vermont for full coverage? Around $1,100. Same coverage. It’s honestly ridiculous when you think about it.

The whole system feels kind of broken sometimes, but understanding WHY rates vary so much actually helps. At least you’ll know if you’re getting screwed or if that’s just… what it costs where you are.

Why your ZIP code matters (probably more than your driving record)

I’m not even exaggerating here. Your address can matter MORE than whether you’ve had accidents. Insurance companies have all this data – and I mean ALL of it – about every single ZIP code in the country. Accident rates, how many cars get stolen, what repairs cost, even how often people sue each other after fender benders.

Cities are brutal for insurance costs. I mean, it makes sense when you think about it – more cars, more traffic, more idiots on their phones, more opportunities for things to go wrong. But the difference is nuts.

My cousin lives in Brooklyn. I live in rural Vermont. We both drive Honda CR-Vs, both have clean records. She pays like $2,800 a year. I pay $1,400.

Actually, that reminds me of when my friend Jake moved from Phoenix to Miami for work last year. He was so excited about the job, got a nice raise and everything. Then he updated his insurance address and his premium jumped from… I think it was around $1,500 to almost $2,800? He called me thinking it was a mistake. Nope. Just Florida being Florida.

Random things that affect your local rates:

- How bad traffic is (obviously)

- Local accident statistics

- Theft rates – and some areas are WAY worse than others

- What body shops charge in your area

- Weather stuff – hurricanes, hail, whatever

- How lawsuit-happy people are in your state (this is a real thing)

- The percentage of uninsured drivers around you

That last one is depressing. In some states, like one in four drivers has NO insurance. Which means you’re basically paying extra to protect yourself from all the irresponsible people who can’t be bothered to follow the law.

Weather is weird too. You wouldn’t think hail would matter that much, but I talked to someone in Colorado who said everyone on their street filed claims the same week after a hailstorm. Insurance companies know this stuff happens and they price it in.

The most expensive states (spoiler: avoid Michigan if you can)

Michigan is the worst. Has been for years. The average premium is over $3,400 a year now – might even be higher depending on where exactly you are. They had this law requiring unlimited lifetime medical coverage that just destroyed rates for decades.

They changed the law a couple years back so you can opt for lower medical coverage if you already have health insurance, but it’s still the most expensive state by a mile.

Here’s roughly how the most expensive states shake out:

| State | Average yearly cost | Why it sucks |

|---|---|---|

| Michigan | ~$3,500 | That medical coverage thing, plus Detroit winters |

| Louisiana | ~$2,800 | Lots of accidents, hurricanes, people sue a lot |

| Florida | ~$2,700 | Hurricanes, fraud, tons of uninsured drivers |

| California | ~$2,550 | Traffic, expensive everything, car theft |

| Nevada | ~$2,500 | Vegas tourists crashing into things |

| New York | ~$2,400 | NYC basically, expensive medical costs |

| Delaware | ~$2,300 | Lawsuit stuff mainly |

| Rhode Island | ~$2,300 | Small state, aggressive drivers |

| Maryland | ~$2,250 | Baltimore crime rates don’t help |

| Kentucky | ~$2,200 | High uninsured rate, rural accidents |

Note: These are estimates from various sources, your actual costs will vary

Louisiana being #2 makes sense when you consider it’s got both severe weather AND a reputation for expensive lawsuits. New Orleans especially pushes that average way up.

Florida’s interesting because it’s a “no-fault” state, which was supposed to REDUCE lawsuit costs and make insurance cheaper. Yeah… that didn’t work. Between hurricanes, insurance fraud (especially in South Florida – that’s been a problem forever), and all the retirees and tourists, Florida’s a mess insurance-wise.

California and Nevada round out the top five. California’s just expensive for everything – cars cost more, repairs cost more, everything costs more. A minor fender bender in LA can cost twice what it would in like, Ohio, just because labor rates are insane.

Nevada’s mainly Vegas and Reno – tourist traffic, drunk drivers, people driving too fast on empty highways and then suddenly there’s traffic. I drove through Vegas once and the number of close calls I saw in like an hour was insane.

The cheapest states (basically anywhere rural and cold)

Vermont’s the cheapest, which is great for me personally. Around $1,100 average for full coverage. Low population, not much traffic, people generally drive okay.

The fall tourist season is annoying – leaf peepers everywhere going 25mph and stopping randomly to take photos – but it doesn’t really affect insurance rates much.

The affordable states:

| State | Average cost | Why it’s cheap |

|---|---|---|

| Vermont | ~$1,100 | Rural, low traffic, responsible drivers mostly |

| Maine | ~$1,150 | Same deal as Vermont |

| New Hampshire | ~$1,175 | Doesn’t even require insurance (weird) |

| Idaho | ~$1,200 | Very rural |

| Ohio | ~$1,300 | Decent balance |

| Iowa | ~$1,325 | Farm state, careful drivers |

| South Dakota | ~$1,350 | Almost nobody lives there |

| North Dakota | ~$1,400 | See above |

| Wyoming | ~$1,400 | Literally the least populated state |

| Wisconsin | ~$1,425 | Good roads, moderate weather |

Maine’s similar to Vermont – rural, not many people, low accident rates. More moose than traffic jams, as they say.

New Hampshire’s weird because they don’t actually require you to have insurance. You just have to prove you can cover costs if you cause an accident. So the people who DO buy insurance tend to be more responsible? I guess? It creates an interesting dynamic.

The pattern’s pretty clear though – rural states in the Great Plains and Mountain West have cheap insurance. Less traffic = fewer accidents = lower costs for everyone.

The difference between Michigan and Vermont is insane when you calculate it out. Like $2,400 MORE per year just for living in Michigan. Over 10 years that’s $24,000 in extra insurance costs just because of your address. You could buy a decent used car with that difference.

How age completely screws young drivers

Okay, so this is where I feel bad for teenagers and their parents. The statistics don’t lie though – young drivers crash WAY more often than everyone else.

If you’re 16-19 years old, you’re looking at an average of like $5,800 a year for full coverage. That’s not a typo. It’s 172% higher than the national average, which is already around $2,150.

Rough breakdown by age:

- 16-19 years old: ~$5,800/year (ouch)

- 20-24: ~$3,300/year (still bad)

- 25-34: ~$2,000/year (getting better)

- 35-44: ~$1,900/year (pretty good)

- 45-54: ~$1,800/year (best rates)

- 55-64: ~$1,750/year (still great)

- 65+: ~$1,900/year (slight increase)

My neighbor’s kid just turned 17 and got his license. Adding him to their insurance cost an extra… I think they said $3,600 a year? Maybe it was $3,800, I can’t remember exactly. Either way, they’re now paying almost $5,000 total for their two cars. They briefly talked about just not insuring him but obviously that’s illegal and financially stupid if he causes an accident.

The logic makes sense even if it feels unfair. Teen drivers have zero experience, their brains literally aren’t fully developed yet (the judgment part doesn’t finish until like 25), and they crash constantly. Insurance companies actually lose money on teen drivers as a group, which is why they charge so much.

Young men get hit even harder than young women. A 19-year-old guy might pay $6,800 while a 19-year-old woman pays $4,900 for the same coverage. That’s almost $2,000 difference just because of gender and statistics.

Although some states banned that practice – California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania don’t allow gender-based pricing anymore.

The big drop happens at 25. I remember when I turned 25, my insurance went down like $400 a year even though nothing else changed. Same car, same record, just got older. It felt like getting a raise honestly.

The sweet spot is basically 25-65. Those are your prime years for cheap insurance. You’ve got experience, you’ve (hopefully) learned not to drive like an idiot, and the statistics show you’re just safer.

After 65 it ticks back up a tiny bit. Reaction times slow down, vision issues, that kind of thing. But it’s not dramatic – maybe goes from $1,750 to $1,900. Still way better than being a teenager.

Tickets and accidents will destroy you

This is the part you actually have control over, and the impact is huge.

A single speeding ticket even a minor one like 12 over – can raise your rates 20-25%. That’s $400-500 MORE per year on average. And it stays on your record for three years usually, so you’re paying an extra $1,200-1,500 total for one mistake.

How violations mess up your rates:

- Speeding (1-15 over): +20-25%, sticks around 3 years

- Speeding (16+ over): +28-35%, lasts 3-5 years

- At-fault accident: +40-50%, haunts you for 3-5 years

- Reckless driving: +70-90%, on record for 5 years

- DUI: +80-150%, follows you 5-7 years

- No insurance ticket: +35-50%, 3 years

Those numbers are rough averages – could be more or less depending on your company and state.

DUIs are catastrophic. I have a friend who got one about three years ago (he’s doing better now, got help and everything). His insurance went from $1,800 to $4,500 a year. SOME companies wouldn’t even cover him – he had to go to a high-risk insurer. He’s still paying elevated rates and will be for another couple years.

He’s told me that one mistake has cost him over $10,000 in extra insurance so far, plus all the legal fees and other consequences. Not worth it, obviously.

At-fault accidents are bad too. You’re looking at 40-50% increase for 3-5 years. An accident that bumps your premium from $2,000 to $3,000 costs you an extra $5,000 over five years.

The good news is that clean records get rewarded. Most companies have safe driver discounts – like 10-20% off if you’ve had no tickets or accidents for 3-5 years. That’s a few hundred bucks saved just for not screwing up.

I’ve had a clean record for… god, probably seven years now? Knock on wood. That discount is one of the reasons my rate’s as low as it is.

What you drive matters (but maybe not how you think)

Obviously a BMW costs more to insure than a Honda Civic. But the reasons are more complicated than just “expensive car = expensive insurance.”

Insurance companies look at repair costs, theft rates, safety ratings, and claim history for every single vehicle model.

Very rough insurance cost estimates by vehicle type:

- Small sedans (Civic, Corolla): ~$1,400-1,500/year

- Mid-size sedans (Camry, Accord): ~$1,600-1,700/year

- Compact SUVs (CR-V, RAV4): ~$1,750-1,850/year

- Full-size trucks (F-150, Silverado): ~$1,900-2,000/year

- Sports cars (Mustang, Camaro): ~$2,400-2,600/year

- Luxury sedans (BMW 5-Series, Audi A6): ~$2,600-2,800/year

- Performance luxury (BMW M5, Mercedes AMG): $3,200+/year

These are super rough – actual costs vary wildly based on trim level, your age, location, all that stuff.

Sports cars get hammered on insurance. A Mustang might run you $2,500 a year because insurance companies know Mustang drivers tend to… drive like they’re in a Mustang. Fair or not, that’s how it works.

Trucks are interesting. F-150s have high theft rates – people steal the tailgates especially. My neighbor’s had his F-150 tailgate stolen TWICE. He just parks in his garage now.

Safety features help though. My truck has automatic emergency braking and I get like a $120 discount for it. Lane departure warning, blind spot monitoring, good airbags – all that stuff can save you 5-10% each.

Luxury cars just cost more for everything. Parts are expensive, labor’s expensive, even oil changes cost more. All that translates to higher insurance claims, so higher premiums.

Credit scores (because apparently that matters too)

This one makes people mad, and I get why. In most states, insurance companies can use your credit score to set your rate. They claim people with better credit file fewer claims, which… maybe? Critics say it just punishes poor people for being poor.

Either way, it’s legal in most places and the impact is significant.

How credit affects rates (roughly):

- Excellent (800+): Normal rates

- Very good (740-799): +10-15%

- Good (670-739): +20-30%

- Fair (580-669): +40-60%

- Poor (below 580): +70-100%

Someone with poor credit might pay literally DOUBLE what someone with excellent credit pays for the exact same coverage. Over time we’re talking thousands in extra costs just because of credit score.

Only four states ban this practice: California, Hawaii, Massachusetts, and Michigan.

I actually improved my credit score from like 680 to 760 over a couple years (paid off debt, fixed some errors on my report, that whole thing). My insurance went down maybe $350 a year? Which was a nice bonus on top of all the other benefits of better credit.

Putting it all together

All these factors combine to create YOUR specific rate, and understanding how they work together helps you figure out if you’re overpaying.

Like, an 18-year-old guy with a speeding ticket driving a Mustang in Miami is going to pay VASTLY more than a 45-year-old woman with a clean record driving a Civic in Vermont. We’re talking maybe $8,000+ vs $1,200.

I’ve seen some truly insane combinations. Young driver in Michigan, sports car, a violation or two, fair credit – you could be pushing $8,000-10,000 a year. At that point you’re almost better off taking Uber everywhere.

Meanwhile, middle-aged driver in Iowa, safe sedan, clean record, good credit – probably $1,100-1,300.

What you can actually control:

The thing is, you CAN’T easily change your age or location. But you CAN:

- Keep your driving record clean (biggest factor you control)

- Improve your credit score over time

- Choose vehicles with better insurance profiles

- Shop around between companies

That last one’s huge. I was paying $1,900 with my old insurer. Same exact coverage with a new company costs $1,400. I saved $500 by spending maybe two hours getting quotes online.

I kick myself for not doing it sooner, honestly. That’s $500 every single year going forward.

If you’re paying way more than average for your age and state, definitely shop around. Different companies weight factors differently, so rates can vary by hundreds or even thousands for the exact same driver.

Final thoughts

Look, auto insurance is expensive and kind of annoying but understanding WHY rates vary so much at least helps you make better decisions.

If you’re young, you’re going to pay more. That’s just reality. If you live in Michigan or Florida or Louisiana, same thing. But keeping a clean record, maintaining good credit, and choosing the right vehicle all help.

And seriously, shop around every year or two. Insurance companies adjust their rates constantly. The cheapest option this year might be expensive next year, or vice versa.

Stay covered, stay safe, and happy driving.