hidden fees in used car deals: 9 charges to refuse

Most buyers walk into a dealership with a number in mind and walk out having paid $1,500 to $3,000 more than that number — without understanding exactly where the extra cost came from. Hidden fees in used car deals are designed to be added late, added fast, and added in an environment where you’re already tired, emotionally invested, and ready to sign.

This isn’t a cynical take on the car business. Most dealers operate legitimately. But the structure of the finance office creates real pressure points where fees can multiply quietly. If you’re new to buying used, the essential used car buying mistakes guide gives you the full map of what can go wrong before and after the price negotiation. Here, the focus is entirely on fees — what they are, which ones you’re legally required to pay, and which ones you can push back on.

hidden fees in used car deals: real vs. invented charges

Let’s be direct about something most car buying guides avoid. There are fees you cannot escape — not because dealers invented them, but because they’re government-mandated. Sales tax, title fee, and registration are set by your state and county. They will appear on every buyer’s order regardless of where you shop. These are non-negotiable.

Everything else — every other line item on that worksheet — is either a dealer cost recovery attempt or a flat-out fabrication. That’s a strong claim, but it holds up. Documentation fees, reconditioning charges, market adjustment fees, VIN etching, advertising recovery, paint protection — none of these are required by any law. They exist because buyers generally accept them.

According to the Federal Trade Commission’s consumer car buying guide, dealers are required to clearly disclose all fees and charges before finalizing any sale. If a line item wasn’t discussed during the price negotiation, you have every right to question it before signing.

Understanding that distinction is the first thing that shifts the power dynamic in your favor.

the doc fee: how much is too much

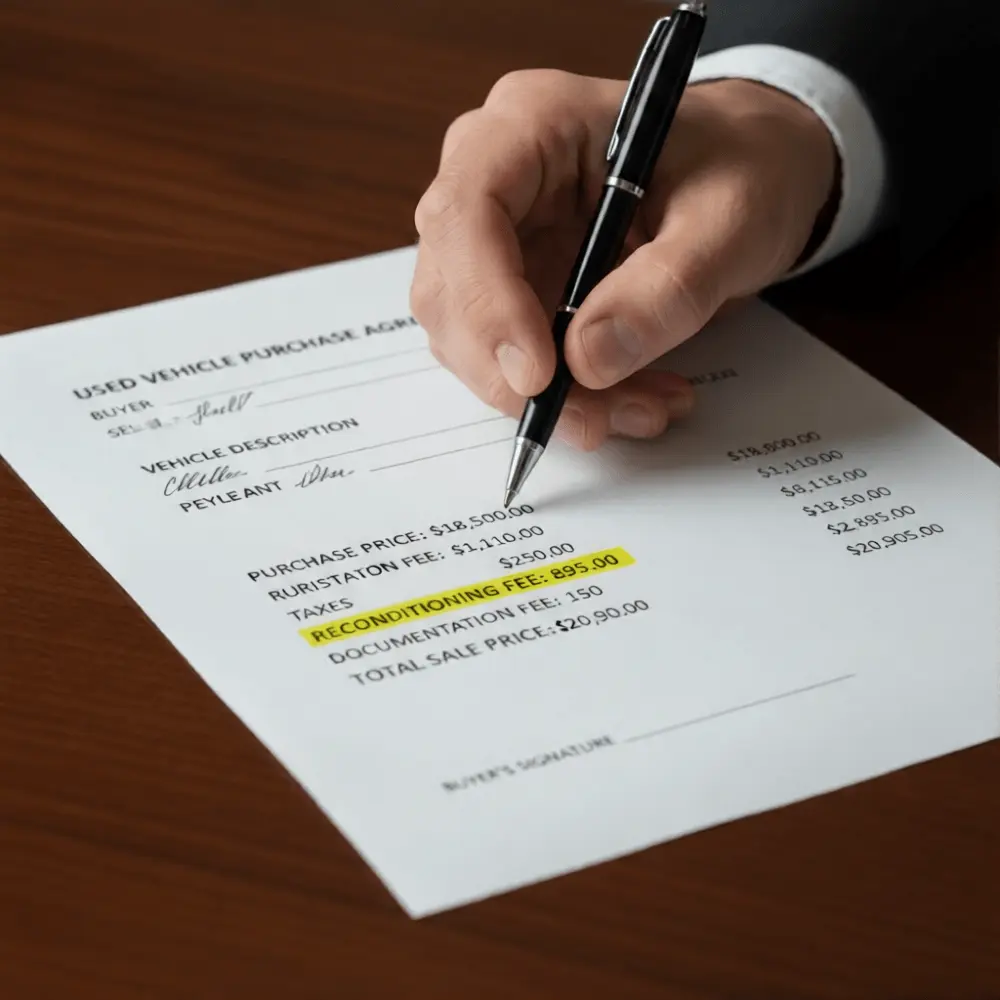

The documentation fee — usually listed as “doc fee” on the buyer’s order — covers the administrative work of processing the sale: title transfer paperwork, DMV filing, and contract preparation. That work is real, and some doc fee is standard practice across the industry.

The problem is the range. California caps it at $85. Other states have no cap at all, and dealers in Florida, Texas, or Georgia routinely charge $700 to $1,100 for the same 20 minutes of administrative work. You can verify typical doc fee ranges by state using Edmunds’ fee breakdown tool, which tracks what dealers charge across the country.

You generally can’t get a dealer to remove the doc fee entirely. What you can do is negotiate the vehicle selling price down by the equivalent amount. If the doc fee is $800 and the market comps support a vehicle price $800 lower, the end result for your wallet is the same.

reconditioning fee: don’t pay for their cost of doing business

A reconditioning fee is what a dealer charges for cleaning the car, topping off fluids, replacing wiper blades, and making minor cosmetic repairs before the vehicle goes on sale. This is a standard part of running a used car operation.

It is not your cost to carry.

Dealers factor reconditioning into their acquisition margin. When a dealership buys a used car at auction, they build reconditioning into what they’re willing to pay, and then into the price they list. Charging a separate reconditioning fee on top of the selling price is effectively billing you twice for the same thing.

Refuse it. Ask the finance manager to remove it from the buyer’s order. If they resist, ask them to reduce the vehicle price by the same amount. One of those two outcomes is reasonable — paying the fee as listed is not.

fees that should never appear on a used car deal

Some charges are questionable on new vehicles. On a used vehicle, they’re completely indefensible. These are among the most common hidden fees in used car deals that buyers pay without realizing they could have refused them entirely.

Destination fee. This covers the cost of shipping a new car from the factory to the dealership. That car is already there. It arrived years ago. A destination fee on a used vehicle is a pure invention. Cross it off.

Dealer preparation fee. Sometimes listed as “PDI” (pre-delivery inspection), this is essentially reconditioning with a different label. Same logic applies — it’s a cost of their business, not yours.

Advertising fee. This appears as a line item covering the dealer’s marketing and advertising spend. There is no universe in which a buyer should absorb a car dealer’s television and Google ad budget. Remove it.

VIN etching fee. This charges $150 to $400 for engraving the vehicle identification number onto windows as a theft deterrent. You can have this done independently for under $30. The dealer version is not worth the markup. Decline it.

| Fee Name | What It Is | Typical Range | What to Do |

|---|---|---|---|

| Doc fee | Paperwork processing | $85–$1,100 | Negotiate vehicle price down by same amount |

| Reconditioning fee | Used car prep and cleaning | $200–$1,000+ | Refuse — built into selling price |

| Destination fee (used) | Factory-to-dealer shipping | $300–$995 | Refuse — car already arrived years ago |

| Dealer prep / PDI fee | Pre-delivery inspection | $200–$600 | Refuse — duplicate of reconditioning |

| VIN etching fee | Theft deterrent engraving | $100–$400 | Decline or source independently for $30 |

| Advertising fee | Dealer marketing cost recovery | $100–$500 | Remove — not your expense |

GAP insurance: the right product, the wrong source

GAP insurance is a product that genuinely exists for a reason. If your car is totaled or stolen and your insurance payout is lower than your remaining loan balance, GAP coverage makes up the difference. That’s a real risk, especially on a loan with a low down payment.

The problem isn’t GAP insurance. The problem is buying it from the dealership.

Dealers routinely charge $400 to $900 for GAP coverage. Your own auto insurer offers the same product — sometimes literally the same product from the same underwriter — for $20 to $40 per year. That difference, financed into a 60-month loan, ends up costing you more than the coverage is ever likely to pay out.

The Consumer Financial Protection Bureau advises buyers to compare all financing add-on products — including GAP insurance — with independent providers before accepting anything presented in the finance office.

Before you enter the finance office, call your auto insurance provider and ask what they charge for GAP coverage. Have that number ready. If the dealer’s version is more than three times the cost, decline and add it to your own policy instead.

extended warranties in the finance office

Extended warranty products deserve a detailed conversation of their own, but they belong here because they’re almost always presented as a fee rather than a product choice.

A finance manager will present a service contract as a monthly payment add-on — “it’s only $42 more per month.” On a 72-month loan, that’s $3,024 before interest. And that’s before you’ve read the exclusions list, which on many dealer-sold contracts is extensive enough to disqualify the majority of real-world repairs.

Never make a warranty decision in the finance office under time pressure. Take the contract home, read every exclusion, and compare it against third-party providers before committing. A good warranty purchased thoughtfully is worth considering. A rushed one is almost always a bad deal.

the APR markup you probably didn’t notice

When a dealer arranges your financing, they act as a middleman between you and the lender. The bank might approve you at 7% APR. The dealer presents you with 9% and pockets the difference over the life of your loan. On a $20,000 loan over 60 months, that 2% difference costs you roughly $1,100.

This isn’t illegal — it’s called dealer reserve, and it’s standard practice. The way to neutralize it is simple: get pre-approved through your bank or credit union before you visit any dealership. Walk in with a rate in hand. If the dealer can beat it, great. If not, you use your own financing and the markup disappears entirely.

what to do at the buyer’s order stage

When the finance manager slides the buyer’s order across the desk, slow down. This is not the moment to skim and sign. Hidden fees in used car deals do their most damage at exactly this point, when buyers are eager to finish and emotionally committed to the vehicle.

Read every line. Ask what each fee is for. If you didn’t discuss it during the price negotiation, ask for it to be removed or credited against the selling price. Write down any item you want removed and ask the manager to initial the change.

Two questions that consistently produce results: “Is this fee required by law?” and “If I declined everything except the vehicle and the government fees, what would my OTD price be?” Both force the dealer to separate real costs from invented ones.

Dealers will sometimes say certain fees are non-negotiable. That’s a sales position, not a legal statement. Government fees — tax, title, registration — are fixed. Everything else is a conversation.

one more layer of risk: the title

Getting the fees right is one major step toward a clean deal. But the buyer’s order is only part of what you need to verify before you hand over a check. The car’s title — its legal ownership record — can carry problems that make the purchase expensive or even invalid, regardless of how well you negotiated the price.

Understanding what used car title problems look like and which ones should end the deal entirely is the natural next step once you’ve got the numbers side under control.