Understanding APR and interest rates on used car loans

Annual Percentage Rate (APR) represents the true cost of borrowing by including interest and fees, while the interest rate only reflects the cost of borrowing the principal. Used car loans typically carry higher APRs than new car financing due to depreciation risk and shorter loan terms. Your credit score, loan duration, vehicle age, and down payment significantly impact your final rate. Understanding these fundamentals helps you evaluate offers and make informed decisions throughout your complete financing journey, potentially saving hundreds monthly on your payment.

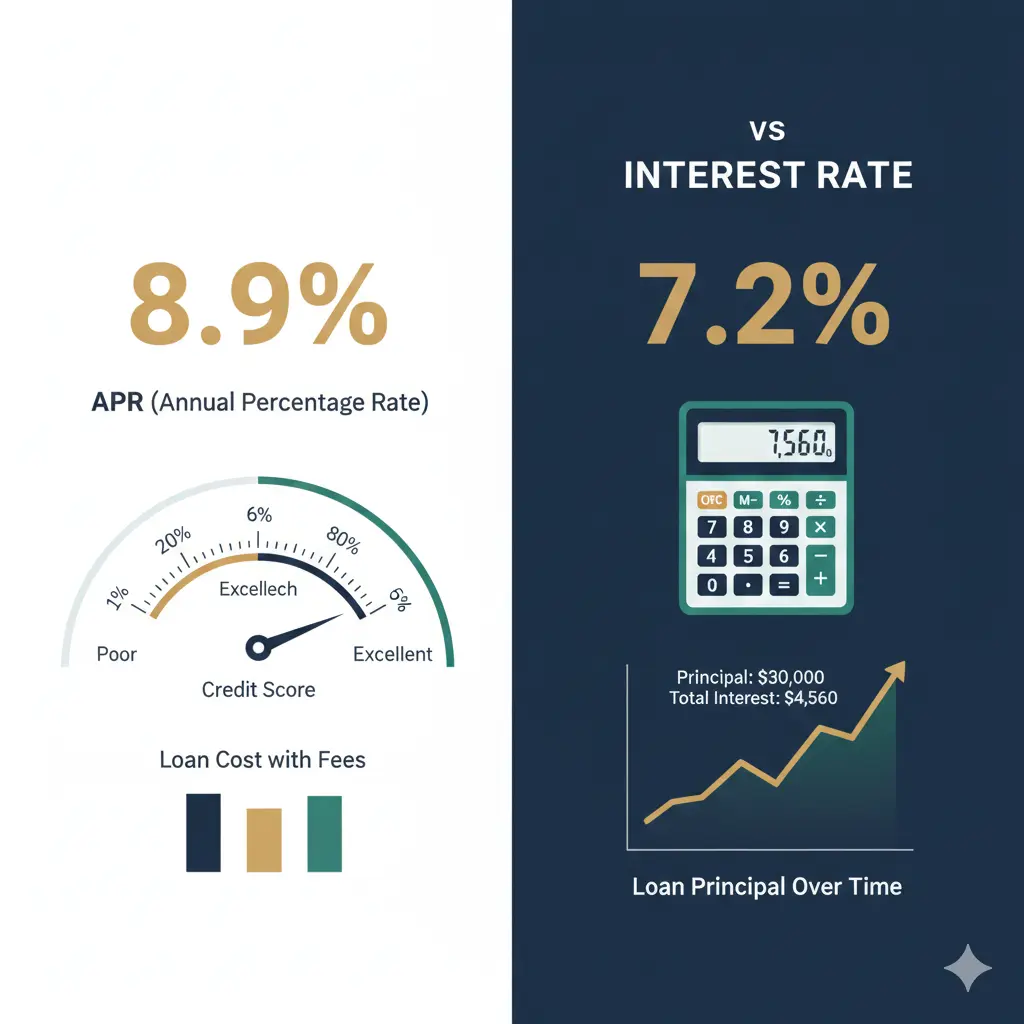

Breaking down APR vs interest rate

The interest rate shows what the lender charges you to borrow money expressed as a yearly percentage. If you borrow $20,000 at 7% interest, you pay roughly $1,400 in interest over the first year before accounting for principal reduction. This number seems straightforward but it doesn’t tell the whole story.

APR includes the interest rate plus other costs like origination fees, documentation fees, and any prepaid finance charges. Lenders must disclose APR by federal law because it gives borrowers a standardized way to compare loan offers. Two lenders might advertise the same interest rate but have different APRs because one charges higher fees.

The difference between interest rate and APR usually ranges from 0.1% to 0.5% on auto loans. Larger gaps signal higher fees that inflate your total cost. Always compare APRs when evaluating multiple offers rather than focusing solely on the interest rate.

Some lenders advertise low rates but bury high fees in the fine print. Others offer competitive APRs with minimal fees but require perfect credit or large down payments. Reading the loan estimate carefully reveals these details before you commit.

What determines your APR

Credit scores drive APR calculations more than any other factor. Lenders categorize borrowers into tiers based on FICO scores with the best rates reserved for scores above 750. Each tier down from there adds percentage points to your rate.

Excellent credit borrowers with scores above 750 might qualify for APRs between 5.5% and 7%. Good credit in the 700-749 range typically sees rates from 7% to 9%. Fair credit scores between 650-699 push rates into the 9% to 12% range. Below 650, you enter subprime territory where APRs can reach 15% to 20% or higher.

The vehicle’s age directly impacts your rate because lenders view older cars as riskier investments. Cars less than three years old often qualify for rates similar to new car financing. Vehicles between four and seven years old see modest rate increases of 1% to 2%. Cars older than eight years face significant rate premiums of 3% or more.

Loan term length creates an inverse relationship with APR. Shorter terms of 36 to 48 months usually carry lower rates than 60 or 72-month loans. Lenders charge more for longer terms because they face extended risk exposure and you’re paying interest for more years.

Down payment size influences your APR because it reduces the lender’s risk. Putting 20% or more down can lower your rate by 0.5% to 1% compared to minimal down payment loans. Some lenders offer special promotions with better rates for borrowers who make substantial down payments.

Current market rates for used car loans

Average APRs for used cars in 2026 range from around 6% for excellent credit to over 18% for poor credit. These rates fluctuate based on Federal Reserve policy and broader economic conditions. When the Fed raises benchmark rates, auto loan APRs typically follow within a few months.

Credit unions consistently offer rates 1% to 2% below banks on average. A credit union might charge 6.5% APR where a bank charges 8% for the same borrower and vehicle. This gap represents real savings over the loan term.

Online lenders fall somewhere between banks and credit unions on pricing. They compensate for lack of physical branches by offering competitive rates and faster processing. However, their rates vary widely based on their risk models and target customer profiles.

Dealer financing through captive lenders can surprise buyers with promotional rates below market averages. Manufacturers occasionally subsidize rates to move inventory but these deals usually apply to certified pre-owned vehicles rather than standard used cars.

Calculating your total interest cost

Understanding how interest accumulates helps you evaluate different loan scenarios. On a $25,000 loan at 8% APR for 60 months, you’ll pay approximately $5,200 in total interest. The same loan at 10% APR costs about $6,625 in interest.

That 2% APR difference means paying $1,425 more over the life of the loan. Monthly payments increase from $507 to $531 which might seem manageable until you multiply it across 60 payments. Small rate differences compound into significant costs.

Loan amortization front-loads interest payments so you pay more interest in early months than later ones. Your first payment on that $25,000 loan might include $167 toward interest and only $340 toward principal. By the final payment, nearly the entire amount reduces principal.

Making extra payments toward principal accelerates payoff and reduces total interest. Even adding $50 per month to your payment can shave months off the loan term and save hundreds in interest. Some lenders charge prepayment penalties though so verify your loan allows extra payments without fees.

Fixed vs variable rate loans

Most auto loans carry fixed rates that remain constant throughout the loan term. You know exactly what you’ll pay each month and can budget accordingly. Fixed rates protect you from market increases but mean you won’t benefit if rates drop significantly.

Variable rate auto loans are less common but some lenders offer them with initially lower rates that adjust periodically. The rate typically ties to a benchmark like the prime rate plus a margin. If the benchmark rises, your payment increases.

Variable rates create uncertainty in your budget because payments can fluctuate. They might make sense if you plan to pay off the loan quickly before rates can increase substantially. However, most borrowers prefer the predictability of fixed rates for auto loans.

Some lenders advertise teaser rates that apply only for an initial period before adjusting higher. Read the terms carefully to understand when and how much your rate might increase. These loans can cost more over time despite appearing cheaper initially.

Improving your rate before applying

Boosting your credit score even 20 to 30 points can move you into a better rate tier. Pay down credit card balances to reduce utilization below 30% of your limits. Dispute any errors on your credit reports because inaccuracies unfairly lower your score.

Waiting a few months while you improve your credit profile might save you thousands over the loan term. Each percentage point reduction on a $20,000 loan saves roughly $600 to $700 in interest over 60 months. That’s worth a short delay if you can manage it.

Shopping during promotional periods can unlock lower rates too. End of quarter or end of year pushes motivate lenders to meet lending targets. They might offer rate discounts or fee waivers to hit their numbers.

Getting a cosigner with excellent credit can dramatically reduce your rate if your own credit needs work. The cosigner shares legal responsibility for the loan which reduces the lender’s risk. This strategy works best for young buyers without established credit history.

Red flags to watch for

Lenders who don’t clearly disclose APR upfront are hiding something. Federal law requires Truth in Lending disclosures but some unscrupulous dealers or lenders obscure the real costs. If you can’t get a straight answer about APR, walk away.

Spot delivery scams involve dealers letting you drive off with the car before financing is finalized. They call days later claiming your financing fell through and pressure you into a worse loan at a higher rate. Always ensure financing is completely approved before taking possession.

Rate markups happen when dealers add percentage points to the rate the lender approved. They pocket the difference as profit without telling you. This practice is legal in many states but unethical. Having pre-approval helps you identify when a dealer quotes you a higher rate than you should qualify for.

Loans with prepayment penalties lock you into the full term even if you want to pay off early. Avoid these because they prevent you from saving on interest through extra payments or refinancing if rates drop.

When to refinance your loan

Refinancing replaces your current loan with a new one at a better rate. This makes sense if rates have dropped since you bought the car or if your credit score has improved significantly. You can also refinance to shorten or extend your loan term.

Wait at least six months after your original loan before refinancing to give your credit score time to recover from the initial inquiry. Most lenders require at least $7,500 to $10,000 remaining on the loan to make refinancing worthwhile.

Calculate break-even points by comparing closing costs against interest savings. If refinancing costs $500 but saves you $75 monthly in interest, you break even after seven months. Any savings after that point represent real money in your pocket.

Market conditions change rapidly so monitoring rates even after you’ve locked in financing can reveal opportunities. If you see rates drop 1% or more below your current APR, run the numbers to see if refinancing makes sense.

Understanding APR mechanics empowers you to negotiate confidently and recognize good deals from bad ones. Once you know what rate you deserve based on your credit profile and the vehicle you’re buying, you can move forward with applications. For buyers facing credit challenges, exploring bad credit used car financing options and strategies reveals alternative paths to affordable transportation even with imperfect credit histories.